Whole life insurance is a type of permanent life insurance that provides lifelong coverage, guaranteed death benefits, fixed premiums, and cash value accumulation. It is commonly used for long-term financial protection, estate planning, wealth transfer, and legacy planning. Individuals seeking permanent coverage and predictable policy features often consider ordinary life insurance as part of their financial strategy.

Whole Life Insurance: Complete Guide to Coverage, Costs, Cash Value & Providers

Whole life insurance is one of the most widely recognized forms of permanent life insurance. Unlike term life insurance, which expires after a specified period, whole life insurance provides lifelong coverage as long as required premiums are paid.

In addition to a guaranteed death benefit, whole life policies include a cash value component that grows over time. Because of these features, whole life insurance is often considered for long-term financial planning, estate preservation, and legacy objectives.

What Is Whole Life Insurance?

Permanent life insurance policy designed to remain in force throughout the insured person’s lifetime, provided premiums are maintained according to policy terms. When evaluating coverage options, consumers often compare the Best Life Insurance policies based on benefits, financial strength, and long-term value, while also reviewing Cheap Car Insurance solutions to help manage overall household insurance costs.

Most whole life policies include:

- Lifetime coverage

- Guaranteed death benefit

- Fixed premium payments

- Guaranteed cash value accumulation

- Potential dividend eligibility (for participating policies)

How Does Whole Life Insurance Work?

Policyholders pay premiums to the insurance company. A portion of each premium funds the insurance protection while another portion contributes to the policy’s cash value.

The insurer invests these funds and guarantees certain policy benefits, including death benefit protection and minimum cash value growth.

Over time, policyholders may access accumulated cash value through withdrawals or policy loans, subject to policy provisions.

Who Should Consider Whole Life Insurance?

- Individuals seeking permanent coverage

- Parents planning long-term family protection

- High-net-worth households

- Business owners

- Estate planning clients

- Individuals seeking guaranteed premiums

- People interested in legacy planning

- Those wanting tax-advantaged cash value growth

Whole Life Insurance vs Other Policy Types

| Feature | Whole Life | Term Life | Universal Life |

|---|---|---|---|

| Coverage Duration | Lifetime | Temporary | Lifetime |

| Cash Value | Yes | No | Yes |

| Premium Stability | Fixed | Fixed During Term | Flexible |

| Death Benefit | Guaranteed | Guaranteed During Term | Variable/Flexible |

| Typical Cost | Higher | Lowest | Moderate to High |

Key Features of Whole Life Insurance

Lifetime Coverage

Whole life insurance generally remains active for the insured’s entire lifetime as long as premiums continue to be paid.

Guaranteed Death Benefit

Beneficiaries receive the policy’s death benefit when the insured dies, subject to policy conditions.

Fixed Premiums

Premiums typically remain level throughout the life of the policy, offering predictability for long-term budgeting.

Cash Value Accumulation

A portion of premiums contributes to a cash value account that grows over time on a tax-advantaged basis.

Potential Dividends

Some participating whole life policies may pay dividends, although dividends are not guaranteed.

Whole Life Insurance Coverage Comparison

| Coverage Type | Purpose | Best For |

|---|---|---|

| Traditional Whole Life | Permanent protection | Long-term family security |

| Participating Whole Life | Potential dividends | Policyholders seeking additional value |

| Limited Pay Whole Life | Accelerated premium schedule | Early premium completion |

| Single Premium Whole Life | One-time premium payment | Estate and wealth planning |

| Final Expense Whole Life | Burial and end-of-life costs | Seniors seeking smaller coverage amounts |

How Much Does Whole Life Insurance Cost?

Whole life insurance premiums are generally higher than term life insurance because coverage lasts for life and includes cash value growth.

| Applicant Profile | Estimated Monthly Premium Range |

|---|---|

| Healthy Adult Age 30 | $150–$500+ |

| Healthy Adult Age 40 | $250–$700+ |

| Healthy Adult Age 50 | $450–$1,200+ |

| Older Applicants | Varies significantly |

Actual premiums vary based on underwriting, policy design, health status, and coverage amount.

Factors Affecting straight life insurance Premiums

- Age at application

- Health history

- Tobacco use

- Coverage amount selected

- Gender (where legally permitted)

- Family medical history

- Occupation

- Lifestyle choices

- Policy riders selected

How Insurers Underwrite Complete Life Insurance

Insurers assess mortality risk before issuing most whole life policies.

Medical Evaluation

Applicants may complete medical questionnaires, lab work, or physical examinations.

Prescription Review

Insurers often evaluate prescription histories as part of underwriting.

Lifestyle Assessment

Smoking, alcohol use, and hazardous hobbies may affect pricing.

Financial Underwriting

Large coverage amounts may require income and asset verification.

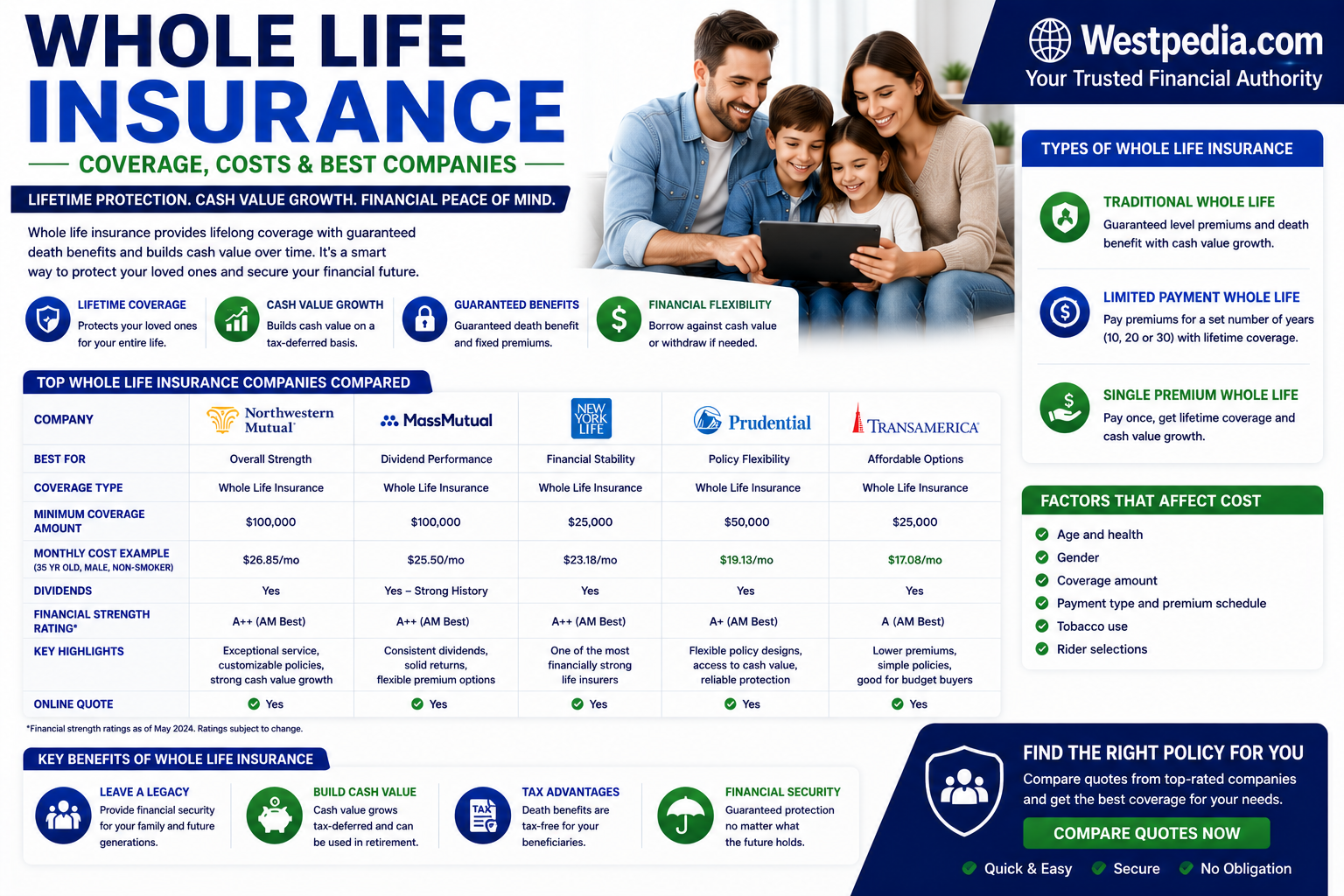

Top Whole Life Insurance Companies

| Insurance Company | Best For | Strengths | Potential Limitations | Pricing Position |

|---|---|---|---|---|

| Northwestern Mutual | Participating whole life | Strong dividend history | Agent-only sales process | Premium |

| MassMutual | Cash value accumulation | Financial strength | Higher costs possible | Premium |

| New York Life | Long-term protection | Broad policy selection | Agent-driven process | Mid to Premium |

| Guardian | Customization options | Flexible rider availability | Availability may vary | Premium |

| Penn Mutual | Permanent coverage solutions | Participating policies | Limited direct purchase options | Premium |

How the Whole Life Insurance Claims Process Works

- The insured person dies.

- Beneficiaries notify the insurance company.

- A claim form is submitted.

- A certified death certificate is provided.

- The insurer reviews policy terms and claim documentation.

- The death benefit is paid if approved.

Advantages of Whole Life Insurance

- Permanent coverage

- Guaranteed death benefit

- Predictable premiums

- Cash value growth

- Potential dividend payments

- Tax-advantaged features

Potential Drawbacks

- Higher premiums than term life insurance

- Complex policy structure

- Long-term commitment

- Cash value growth may take time

- Surrender charges may apply

Common Mistakes When Buying Whole Life Insurance

- Purchasing more coverage than affordable

- Failing to compare multiple insurers

- Not understanding policy illustrations

- Confusing guaranteed and non-guaranteed values

- Ignoring long-term premium obligations

Expert Considerations Before Buying

Prospective buyers should evaluate financial objectives, estate planning goals, cash flow needs, risk tolerance, and long-term affordability before purchasing whole life insurance.

Reviewing policy guarantees, rider options, dividend assumptions, and insurer financial strength can help support informed decision-making.

Frequently Asked Questions

1. What is whole life insurance?

This life insurance is permanent life insurance that offers lifetime coverage, fixed premiums, and cash value accumulation.

2. Does Cash value life insurance expire?

Generally, full life insurance remains in force for life as long as premiums are paid according to policy terms.

3. Is Lifetime life insurance worth it?

Suitability depends on financial goals, budget, and long-term planning needs.

4. Can I borrow against my policy?

Many policies permit loans against available cash value, subject to policy provisions.

5. Are dividends guaranteed?

No. Dividends on participating policies are typically not guaranteed.

6. Is whole life better than term life?

Neither policy type is universally better; each serves different financial objectives.

7. How quickly does cash value grow?

Growth varies by insurer, policy design, and premium structure.

8. Are premiums fixed?

Most traditional whole life policies feature fixed premiums.

9. Can I surrender my policy?

Policies may generally be surrendered, although fees and tax implications may apply.

10. Is a medical exam required?

Many traditional whole life policies require underwriting, although no-exam options exist.

Related Topics

- Term Life Insurance

- Universal Life Insurance

- Final Expense Insurance

- No-Exam Life Insurance

- Estate Planning Strategies