Term life insurance is a type of life insurance that provides coverage for a specific period, such as 10, 20, or 30 years. If the insured dies during the policy term, beneficiaries receive a death benefit. Term life insurance is often chosen for income replacement, debt protection, and family financial security because it typically offers higher coverage amounts at lower premiums than permanent life insurance.

Term Life Insurance: Complete Guide to Coverage, Costs, Quotes & Top Providers

Term life insurance is one of the most popular and affordable forms of life insurance available. Unlike permanent policies, Temporary life insurance provides financial protection for a predetermined period, making it a common choice for families, homeowners, and individuals seeking income replacement protection.

Because premiums are generally lower than permanent life insurance, many consumers use term policies to protect loved ones during their highest financial responsibility years.

What Is Term Life Insurance?

Term life insurance is a temporary life insurance policy designed to provide coverage for a specific period, known as the term. Common term lengths include 10, 15, 20, and 30 years.

If the insured dies while the policy is active, the insurer pays the death benefit to designated beneficiaries. If the policy expires before the insured dies, coverage generally ends unless the policy is renewed, converted, or extended according to policy provisions.

How Does Term Life Insurance Work?

Policyholders pay premiums regularly in exchange for life insurance protection during the selected term period.

Most term policies offer:

- Guaranteed death benefit during the policy term

- Level premiums for a specified period

- Coverage amounts ranging from modest to substantial limits

- Optional riders for additional protection

Unlike whole life insurance, traditional term life policies generally do not accumulate cash value.

Who Should Consider Term Life Insurance?

- Parents with dependent children

- Married couples

- Homeowners with mortgages

- Individuals with significant debts

- Primary household earners

- Young families seeking affordable coverage

- Business owners needing temporary protection

- Individuals seeking income replacement coverage

Why Term Life Insurance Matters

The death of a primary income earner can create significant financial hardship. Temporary life insurance can help surviving family members maintain financial stability by providing funds to:

- Replace lost income

- Pay mortgage obligations

- Cover daily living expenses

- Pay outstanding debts

- Fund children’s education expenses

- Cover funeral and final expenses

- Maintain long-term financial goals

Term Life Insurance Coverage Comparison

| Feature | Term Life Insurance | Whole Life Insurance | Universal Life Insurance |

|---|---|---|---|

| Coverage Duration | 10-30 Years | Lifetime | Lifetime |

| Cash Value | No | Yes | Yes |

| Premium Cost | Lowest | Higher | Moderate to High |

| Death Benefit | Guaranteed During Term | Guaranteed | Flexible |

| Best For | Temporary protection | Permanent coverage | Flexible permanent protection |

Types of Term Life Insurance

Level Term Life Insurance

Level term policies maintain the same premium and death benefit throughout the coverage period.

Decreasing Term Life Insurance

Coverage decreases over time and is often used for mortgage protection purposes.

Renewable

Fixed-Period life insurance

These policies may allow renewal at the end of the term without additional medical underwriting, although premiums often increase.

Convertible Temporary life insurance

Convertible policies allow policyholders to convert temporary coverage into permanent life insurance under specified conditions.

How Much Does Term Life Insurance Cost?

Fixed-Period life insurance depend on age, health, lifestyle, coverage amount, and policy duration.

| Applicant Profile | Risk Level | Estimated Monthly Premium Range |

|---|---|---|

| Healthy Adult Age 30 | Low | $15–$40+ |

| Healthy Adult Age 40 | Moderate | $25–$70+ |

| Healthy Adult Age 50 | Moderate to High | $60–$180+ |

| Smokers or High-Risk Applicants | High | Varies significantly |

Actual premiums vary based on insurer underwriting guidelines and individual risk characteristics.

Factors Affecting Term Life Insurance Premiums

- Age at application

- Health history

- Tobacco and nicotine use

- Coverage amount selected

- Policy term length

- Family medical history

- Occupation

- Dangerous hobbies or activities

- Driving history

- Gender (where legally permitted)

How Insurers Underwrite Term Life Insurance

Life insurers evaluate mortality risk before issuing most policies.

Medical History Review

Insurers examine past and current medical conditions, prescriptions, and treatment history.

Lifestyle Evaluation

Smoking, excessive alcohol consumption, and hazardous activities may increase premiums.

Medical Examination

Some applicants may complete blood work, urine tests, or physical examinations, although no-exam options are available from some insurers.

Financial Review

Large coverage requests may require verification of income and financial obligations.

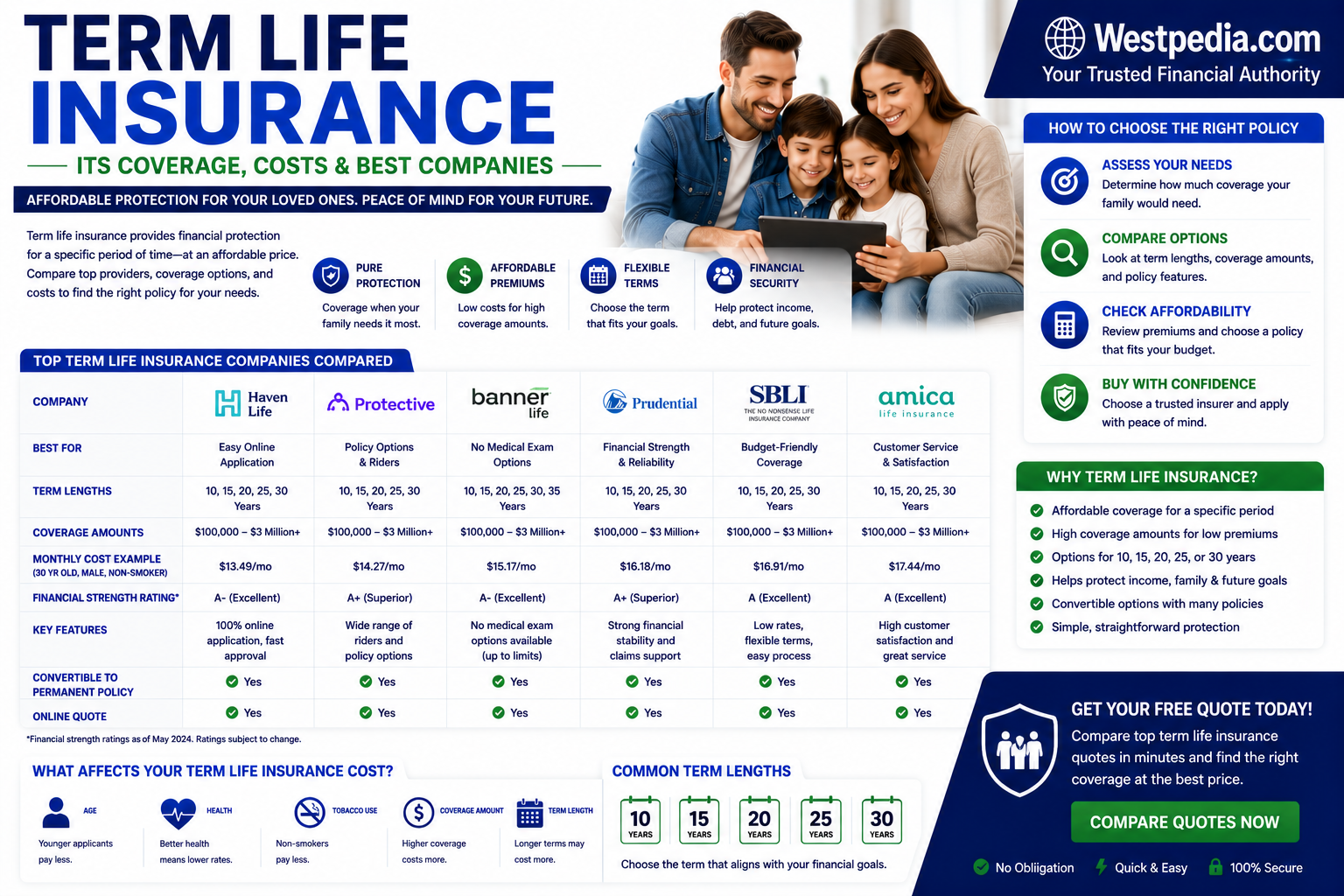

Top Term Life Insurance Companies

| Insurance Company | Best For | Coverage Strengths | Potential Limitations | Pricing Position |

|---|---|---|---|---|

| Banner Life | Competitive pricing | Affordable term products | Limited permanent products | Competitive |

| Protective | Long-term coverage | Broad term options | Online experience varies | Competitive |

| Prudential | Complex underwriting cases | Flexible underwriting | Pricing varies | Mid-range |

| Pacific Life | Policy flexibility | Strong conversion options | Limited direct sales | Mid-range |

| MassMutual | Financial strength | Strong insurer reputation | Premiums may be higher | Premium |

How the Term Life Insurance Claims Process Works

- The insured person dies while coverage is active.

- The beneficiary contacts the insurance company.

- A claim form is completed and submitted.

- A certified death certificate is provided.

- The insurer reviews policy status and claim documentation.

- The death benefit is paid if claim requirements are satisfied.

How to Reduce Term Life Insurance Costs

- Purchase coverage at a younger age

- Maintain good health

- Avoid tobacco products

- Compare quotes from multiple insurers

- Select an appropriate coverage amount

- Consider level term coverage

- Review policy needs periodically

Common Mistakes When Buying Term assurance

- Buying insufficient coverage

- Selecting a term period that is too short

- Waiting too long to apply

- Focusing solely on price

- Failing to compare multiple insurers

- Not reviewing conversion options

Expert Considerations Before Buying

Before requesting quotes, assess your household income, debt obligations, family needs, mortgage balance, education funding goals, and long-term financial responsibilities.

Comparing term lengths, insurer financial strength, conversion privileges, and premium affordability can help support informed decisions. Evaluating the Best Life Insurance options available can help consumers identify policies that align with their coverage needs, budget, and long-term financial goals.

Frequently Asked Questions

1. What is term life insurance?

Term life insurance provides coverage for a specified period and pays a death benefit if the insured dies during the policy term.

2. Does Fixed-Period life insurance

build cash value?

Traditional Term assurance policies generally do not accumulate cash value.

3. How long does term life insurance last?

Common terms include 10, 15, 20, and 30 years.

4. Can I convert Fixed-Period life insurance to permanent insurance?

Many policies include conversion privileges, subject to policy conditions.

5. What happens when the policy expires?

Coverage generally ends unless the policy is renewed or converted.

6. Is Term assurance cheaper than whole life insurance?

Term life insurance is typically less expensive because it provides temporary coverage and does not include cash value.

7. How much Fixed-Period life insurance do I need?

Coverage needs depend on income replacement goals, debts, dependents, and financial obligations.

8. Can seniors buy Term assurance?

Many insurers offer term policies for older applicants, although availability and pricing vary.

9. Is a medical exam required?

Some insurers require medical underwriting, while others offer no-exam policies.

10. Are life insurance proceeds taxable?

Death benefits are often tax-advantaged, although individual circumstances may differ.

Related Topics

- Whole Life Insurance

- Universal Life Insurance

- No-Exam Life Insurance

- Life Insurance Quotes

- Estate Planning