Indexed universal life insurance (IUL) is a permanent life insurance policy that combines lifelong coverage with cash value growth linked to a market index, such as the S&P 500. IUL policies offer flexible premiums and tax-advantaged cash value accumulation, making them attractive for long-term protection, retirement planning, and estate planning strategies.

Indexed Universal Life Insurance: Complete Guide to Coverage, Costs & Providers

Indexed universal life insurance (IUL) is a form of permanent life insurance that provides lifelong coverage while allowing policyholders to build cash value tied to the performance of a market index. Because of its flexibility and growth potential, IUL has become a popular option among individuals seeking both insurance protection and long-term financial planning opportunities.

Unlike term life insurance, IUL policies can remain in force for life if adequately funded. Unlike traditional universal life insurance, cash value growth is linked to an external market index rather than a fixed interest rate.

What Is Indexed Universal Life Insurance?

Indexed universal life insurance is a permanent life insurance policy that includes:

- Lifelong death benefit protection

- Flexible premium payments

- Cash value accumulation

- Index-linked growth potential

- Tax-advantaged policy features

Although policy performance is tied to a market index, cash values are not directly invested in the stock market.

How Does IUL Insurance Work?

A portion of each premium pays insurance costs and fees, while the remainder is allocated to the policy’s cash value account.

Cash value growth is generally linked to indexes such as:

- S&P 500

- NASDAQ-100

- Dow Jones Industrial Average

Most policies include:

- Participation rates

- Performance caps

- Guaranteed minimum floors

These features determine how much interest is credited to the policy.

Who Should Consider Indexed Universal Life Insurance?

- Individuals seeking permanent coverage

- High-income earners

- Business owners

- Estate planning clients

- People seeking tax-advantaged accumulation

- Individuals comfortable with policy complexity

- Long-term retirement planners

Why People Buy IUL Policies

- Lifelong financial protection

- Potential cash value growth

- Flexible premium structures

- Supplemental retirement income strategies

- Estate and legacy planning

- Tax-efficient wealth transfer

Coverage Comparison Table

| Feature | Indexed Universal Life | Whole Life | Term Life |

|---|---|---|---|

| Coverage Duration | Lifetime | Lifetime | Temporary |

| Cash Value | Yes | Yes | No |

| Premium Flexibility | High | Low | Low |

| Growth Potential | Moderate to High | Guaranteed | None |

| Policy Complexity | High | Moderate | Low |

How Much Does Indexed Universal Life Insurance Cost?

| Applicant Profile | Estimated Monthly Premium Range |

|---|---|

| Healthy Adult Age 30 | $150–$400+ |

| Healthy Adult Age 40 | $250–$700+ |

| Healthy Adult Age 50 | $400–$1,200+ |

| Higher-Risk Applicants | Varies significantly |

Actual premiums vary depending on underwriting results, funding goals, insurer pricing, and policy design.

Factors That Affect IUL Premiums

- Age

- Health status

- Smoking history

- Coverage amount

- Funding strategy

- Policy riders

- Family medical history

- Occupation

- Lifestyle risks

How Insurers Underwrite IUL Policies

Medical Evaluation

Most applicants undergo health assessments, questionnaires, and possibly medical exams.

Financial Underwriting

Insurers review income and assets to confirm coverage amounts are appropriate.

Lifestyle Review

Activities such as aviation, scuba diving, or tobacco use may increase premiums.

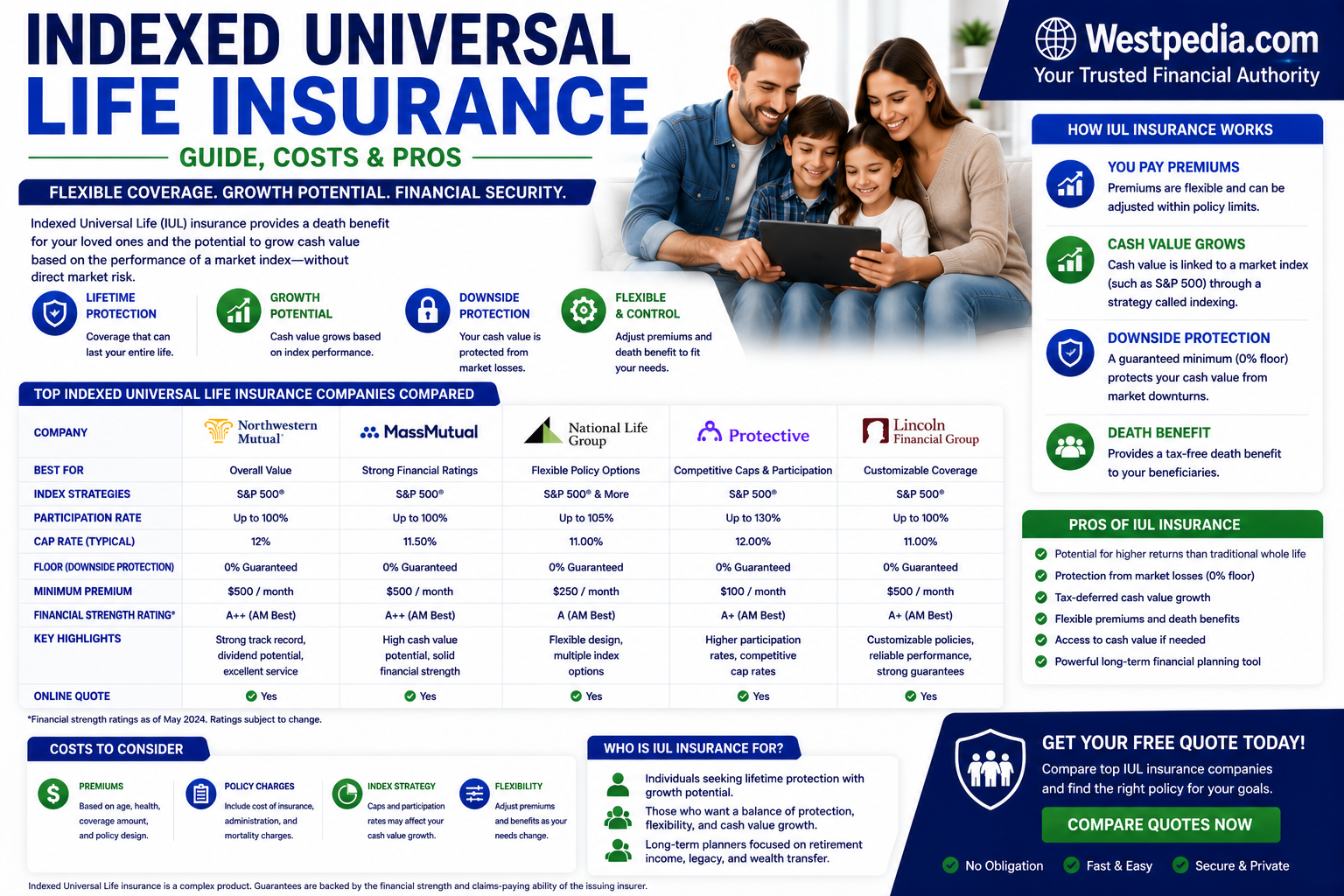

Top Indexed Universal Life Insurance Companies

| Company | Best For | Strengths | Limitations | Pricing Position |

|---|---|---|---|---|

| Nationwide | IUL specialists | Strong indexed products | Complex features | Mid to Premium |

| Pacific Life | Policy flexibility | Broad customization | Agent distribution | Mid-range |

| John Hancock | Wellness incentives | Health rewards programs | Higher costs possible | Premium |

| Lincoln Financial | Retirement strategies | Robust IUL portfolio | Policy complexity | Mid-range |

| Protective | Competitive pricing | Affordable options | Limited online purchasing | Competitive |

Advantages of Indexed Universal Life Insurance

- Permanent coverage potential

- Flexible premiums

- Tax-deferred cash value growth

- Downside protection through policy floors

- Potential for higher returns than fixed universal life

- Access to policy loans and withdrawals

Potential Risks and Drawbacks

- Complex policy structure

- Higher fees than term insurance

- Growth caps may limit returns

- Policy lapse risk if underfunded

- Illustrations are not guarantees

How the Claims Process Works

- Beneficiaries notify the insurer.

- A claim form is completed.

- A death certificate is submitted.

- The insurer reviews documentation.

- The death benefit is paid if claim requirements are met.

How to Reduce IUL Costs

- Apply while young and healthy.

- Avoid tobacco use.

- Compare multiple insurers.

- Review policy funding annually.

- Purchase only the coverage amount needed.

Common Mistakes to Avoid

- Focusing only on projected returns

- Underfunding the policy

- Ignoring annual policy reviews

- Misunderstanding caps and participation rates

- Assuming illustrations are guaranteed

Frequently Asked Questions

1. What is indexed universal life insurance?

It is permanent life insurance with cash value growth linked to a market index.

2. Is IUL insurance invested directly in the stock market?

No. Cash values are credited based on index performance rather than direct market investments.

3. Can I lose money in an IUL?

Most policies include a floor that limits negative interest crediting, but fees and policy expenses still apply.

4. Is IUL better than whole life insurance?

Suitability depends on individual goals, risk tolerance, and financial needs.

5. Can I borrow from an IUL policy?

Many policies allow loans and withdrawals against accumulated cash value.

6. Does IUL provide lifelong coverage?

Yes, provided the policy remains sufficiently funded.

7. Are IUL premiums fixed?

Most IUL policies offer flexible premium options.

8. Is a medical exam required?

Many insurers require underwriting, although some no-exam options exist.

9. Who should buy an IUL policy?

Individuals seeking permanent coverage with cash value growth potential may consider IUL insurance.

10. Are policy illustrations guaranteed?

No. Future policy performance may differ from illustrations.

Related Topics

- Universal Life Insurance

- Whole Life Insurance

- Term Life Insurance

- No-Exam Life Insurance

- Retirement Income Planning