Low interest credit cards can help consumers reduce borrowing costs when carrying balances from month to month. While rewards and welcome bonuses often attract attention, the annual percentage rate (APR) becomes one of the most important factors for cardholders who do not consistently pay balances in full.

Whether you need to finance a major purchase, consolidate existing debt, or minimize interest expenses, comparing low interest credit cards carefully can potentially save hundreds or even thousands of dollars over time.

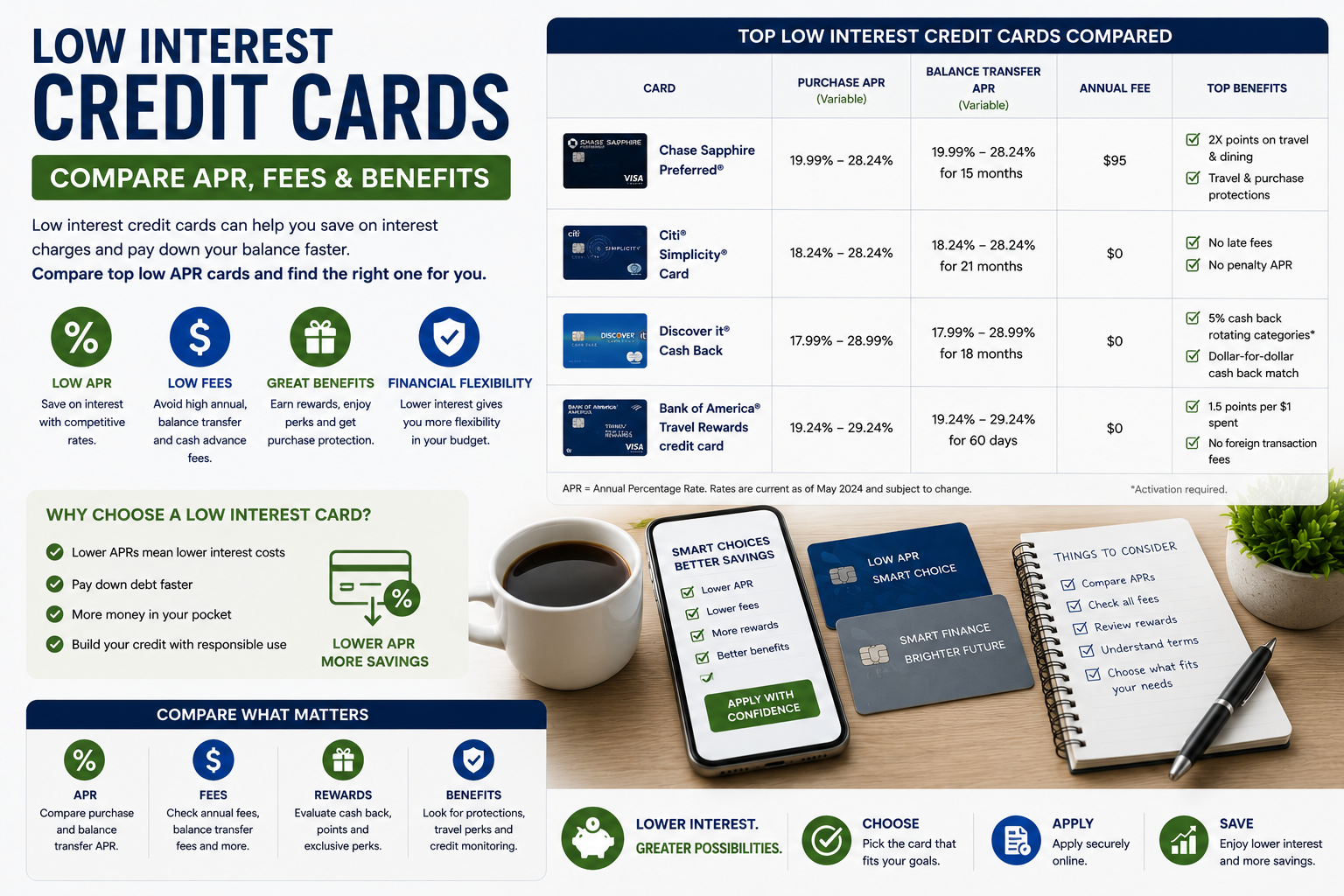

Low Interest Credit Cards Complete Guide

Low interest credit cards typically offer:

- Lower ongoing purchase APRs

- Introductory 0% APR promotions

- Balance transfer opportunities

- Reduced financing costs

- Lower total borrowing expenses

- Flexible repayment options

Consumers who routinely carry balances often prioritize APR over rewards because interest charges can significantly reduce or eliminate reward value.

Who Should Consider Low Interest Credit Cards?

Low interest credit cards may be appropriate for:

- Consumers financing large purchases

- Individuals consolidating higher-rate debt

- Cardholders carrying occasional balances

- Consumers seeking introductory financing offers

- Borrowers focused on minimizing interest costs

Consumers who consistently pay balances in full each month may benefit more from rewards-focused products instead.

What Financial Need Do Low Interest Credit Cards Solve?

These cards primarily help consumers:

- Reduce interest expenses

- Manage short-term financing needs

- Pay down existing credit card debt

- Avoid high borrowing costs

- Finance planned purchases more affordably

How Low Interest Credit Cards Work

When cardholders carry balances beyond the statement due date, interest is generally charged based on the card’s APR.

Low interest cards attempt to reduce these charges by offering:

- Lower standard variable APRs

- Promotional 0% APR periods

- Reduced balance transfer rates

After promotional periods expire, standard variable APRs typically apply.

Low Interest Credit Card Features Comparison Table

| Feature | Details |

|---|---|

| Introductory APR | Temporary reduced or 0% APR offer |

| Ongoing APR | Variable rate after promotional period |

| Balance Transfer Option | Ability to transfer existing debt |

| Annual Fee | May range from $0 to premium pricing |

| Rewards Program | Some cards include cash back or points |

| Purchase Protection | Coverage on eligible purchases |

| Fraud Protection | Protection against unauthorized use |

| Account Management Tools | Digital budgeting and payment features |

APR Types Consumers Should Compare

| APR Type | Purpose |

|---|---|

| Purchase APR | Interest on purchases |

| Balance Transfer APR | Interest on transferred balances |

| Cash Advance APR | Interest on cash withdrawals |

| Penalty APR | Higher APR triggered by certain events |

Understanding Introductory APR Offers

Many low interest cards provide promotional financing periods that may last from several months to more than a year.

Common promotional offers include:

- 0% APR on purchases

- 0% APR on balance transfers

- Reduced introductory rates

Consumers should understand:

- Promotional expiration dates

- Standard APR after promotion ends

- Balance transfer deadlines

- Applicable transfer fees

Example Interest Cost Comparison

| Balance | APR | Estimated Annual Interest* |

|---|---|---|

| $5,000 | 18% | $900 |

| $5,000 | 24% | $1,200 |

| $5,000 | 30% | $1,500 |

*Illustrative estimates assuming balance remains unpaid for one year. Actual costs vary.

Fees and Total Cost of Ownership

APR is important, but additional fees also affect total borrowing costs.

| Fee Type | Typical Range |

|---|---|

| Annual Fee | $0–$150+ |

| Balance Transfer Fee | 3%–5% |

| Cash Advance Fee | 3%–5% |

| Foreign Transaction Fee | 0%–3% |

| Late Payment Fee | Issuer dependent |

Annual Fees

Many low interest cards charge no annual fee, although some premium products include fees in exchange for enhanced benefits.

Balance Transfer Fees

Most issuers charge a fee equal to approximately 3% to 5% of the transferred balance.

Penalty APR Considerations

Missed payments or account defaults may trigger higher penalty APRs on certain products.

Rewards and Benefits Analysis

Low interest cards may offer rewards, although earning rates are sometimes lower than premium rewards cards.

| Reward Category | Typical Earnings Rate |

|---|---|

| General Spending | 1%–2% |

| Dining | 1%–3% |

| Travel | 1x–3x points |

| Groceries | 1%–3% |

| Gas Purchases | 1%–3% |

Consumers carrying balances should generally prioritize APR savings over maximizing rewards.

Credit Score Requirements

| Credit Profile | Typical FICO Range | Approval Outlook |

|---|---|---|

| Poor | 300–579 | Limited options available |

| Fair | 580–669 | Entry-level low APR products |

| Good | 670–739 | Broad product availability |

| Very Good | 740–799 | Competitive low APR offers |

| Excellent | 800–850 | Access to premium low-rate products |

Issuer Comparison Table

| Issuer | Best For | Typical Credit Needed |

|---|---|---|

| Chase | Flexible financing and rewards | Good to Excellent |

| American Express | Premium financing features | Good to Excellent |

| Capital One | Straightforward borrowing products | Fair to Excellent |

| Citi | Balance transfer products | Good to Excellent |

| Discover | Long intro APR offers | Fair to Good |

| Bank of America | Relationship banking benefits | Good to Excellent |

| Wells Fargo | Introductory APR promotions | Good to Excellent |

Issuer Insights

Chase

Strengths: Flexible rewards ecosystem and financing options.

Weaknesses: Competitive approval standards.

American Express

Strengths: Strong customer experience and premium benefits.

Weaknesses: Some cards include annual fees.

Citi

Strengths: Historically strong balance transfer offerings.

Weaknesses: Benefits vary across products.

Discover

Strengths: Introductory financing opportunities and accessible products.

Weaknesses: Smaller portfolio compared with major issuers.

Application and Underwriting Factors

- Credit score

- Credit utilization ratio

- Payment history

- Debt-to-income ratio

- Existing account relationships

- Recent credit inquiries

- Income verification

- Length of credit history

Approval Process Explained

1. Application Submission

Applicants provide financial and personal information.

2. Credit Review

The issuer reviews credit reports and risk indicators.

3. Underwriting Assessment

Repayment ability and creditworthiness are evaluated.

4. Approval or Denial

The issuer determines eligibility.

5. Card Issuance Timeline

Approved applicants typically receive cards within several business days.

6. Activation Process

The card must be activated before use.

How to Improve Approval Odds

- Pay bills on time.

- Lower credit utilization.

- Review credit reports for errors.

- Limit unnecessary applications.

- Apply for cards suited to your credit profile.

How to Avoid Interest Charges

- Pay statement balances in full whenever possible.

- Make payments before due dates.

- Avoid cash advances.

- Track promotional APR expiration dates.

Common Credit Card Mistakes

- Ignoring APR after introductory periods end.

- Missing payments.

- Carrying high balances.

- Overspending because of available credit.

- Using cash advances unnecessarily.

Benefits vs Risks

Benefits

- Reduced borrowing costs

- Potential introductory financing

- Debt management flexibility

- Purchase protections

- Possible rewards earnings

Risks

- High standard APRs after promotional periods

- Balance transfer fees

- Overspending risks

- Potential credit score damage from missed payments

- Debt accumulation

Alternatives to Consider

- Balance transfer credit cards

- Personal loans

- Home equity products

- Rewards credit cards

- Secured credit cards

Expert Considerations

Consumers who expect to carry balances often benefit more from low APR products than high-reward cards. Even small APR differences can produce meaningful savings over time. Compare ongoing APRs, promotional periods, fees, and total borrowing costs before applying.

Approval is not guaranteed. APRs, promotional offers, and fees may change without notice. Always review official issuer disclosures before submitting an application.

Frequently Asked Questions

1. What is a low interest credit card?

A credit card offering lower borrowing costs through reduced APRs or promotional financing periods.

2. What APR is considered low?

Definitions vary, but rates below industry averages are often considered comparatively low.

3. Are low interest cards better than rewards cards?

It depends on spending habits and whether balances are carried.

4. Can I get a low APR card with fair credit?

Some issuers offer products for consumers with fair credit, although terms may vary.

5. What happens when a 0% APR period ends?

The card’s standard variable APR typically applies.

6. Do balance transfers affect credit scores?

They may affect utilization ratios and overall credit profiles.

7. Are balance transfer fees common?

Yes, many issuers charge transfer fees.

8. Does applying affect credit scores?

Applications often result in hard inquiries.

9. Can I avoid interest completely?

Paying statement balances in full generally avoids purchase interest.

10. How long does approval take?

Some decisions are instant, while others require manual review.

11. Can low interest cards help with debt repayment?

They may assist some consumers when used responsibly.

12. Is approval guaranteed with good credit?

No. Issuers evaluate multiple underwriting factors.

Related Topics

- Best Cash Back Credit Cards

- Credit Card Comparison

- Balance Transfer Credit Cards

- Travel Rewards Programs

- Credit Card APR Explained