A home loan is a mortgage used to purchase, refinance, or improve residential property. Home loans allow borrowers to spread the cost of a home over many years while making monthly payments. Prospective homebuyers, homeowners refinancing existing mortgages, and individuals purchasing residential property should compare rates, fees, and qualification requirements before applying.

Home Loan Guide Rates, Requirements & Best Lenders

Buying a home is one of the largest financial decisions most people will ever make. Because few buyers can purchase property entirely with cash, home loans play a critical role in making homeownership possible.

A home loan, also known as a mortgage, allows borrowers to finance the purchase of residential real estate and repay the balance over time through scheduled monthly payments.

What Is a Home Loan?

A home loan is a secured mortgage used to purchase, refinance, or renovate residential property. The property itself serves as collateral for the loan.

Home loans are commonly used to purchase:

- Primary residences

- Single-family homes

- Condominiums

- Townhouses

- Multi-unit owner-occupied properties

- Vacation homes

Who Should Consider a Home Loan?

- First-time homebuyers

- Repeat homebuyers

- Homeowners refinancing existing mortgages

- Borrowers purchasing vacation homes

- Individuals building long-term wealth through homeownership

What Financial Problem Does a Home Loan Solve?

Home loans allow borrowers to purchase property without paying the entire purchase price upfront. Financing can help buyers:

- Become homeowners sooner.

- Preserve savings and liquidity.

- Spread housing costs over many years.

- Build home equity gradually.

- Refinance to lower monthly payments.

Typical Home Loan Rates, Costs & Terms

| Feature | Typical Range |

|---|---|

| Loan Amount | $50,000 to several million dollars |

| APR | 5.50% – 8.50% |

| Loan Terms | 10 to 30 years |

| Down Payment | 3% – 20%+ |

| Origination Fees | 0% – 2% |

| Closing Costs | 2% – 6% of purchase price |

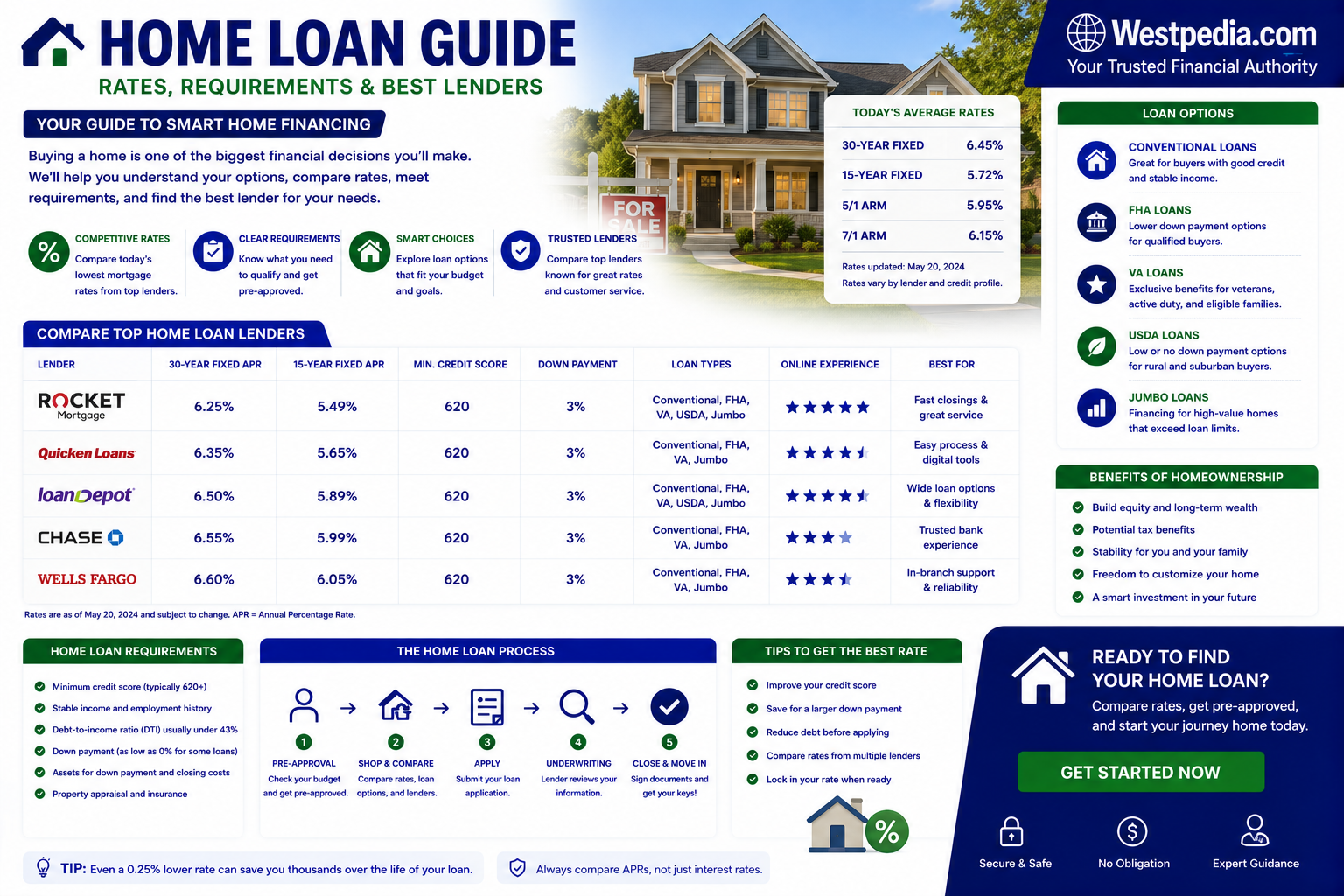

Types of Home Loans

| Loan Type | Best For | Key Features |

|---|---|---|

| Conventional Loan | Strong-credit borrowers | Competitive rates and flexible terms |

| FHA Loan | First-time buyers | Lower down payment requirements |

| VA Loan | Eligible military borrowers | No down payment for qualified borrowers |

| USDA Loan | Eligible rural homebuyers | Low or no down payment options |

| Jumbo Loan | Higher-priced properties | Larger borrowing limits |

| Fixed-Rate Mortgage | Predictable payments | Stable interest rate throughout term |

| Adjustable-Rate Mortgage | Short-term ownership plans | Rate may change periodically |

How Much Home Loan Can You Afford?

Lenders generally evaluate:

- Monthly income

- Debt-to-income ratio (DTI)

- Existing debt obligations

- Down payment amount

- Credit history

- Cash reserves

Many lenders prefer total monthly debt obligations to remain below established DTI thresholds, although requirements vary.

Factors That Influence Home Loan Rates

- Credit Score: Higher scores may qualify for lower rates.

- Debt-to-Income Ratio: Lower DTI often improves pricing.

- Down Payment: Larger down payments may reduce risk.

- Loan Term: Shorter terms often carry lower rates.

- Property Type: Primary residences usually receive better pricing.

- Loan Amount: Jumbo loans may have different pricing structures.

- Geographic Location: Market conditions may influence availability.

Best Home Loan Lenders Compared

| Lender | Best For | Strengths | Potential Limitations |

|---|---|---|---|

| Bank of America | Relationship banking customers | Extensive mortgage programs | Detailed documentation process |

| Wells Fargo | Traditional borrowers | Large branch network | Qualification standards vary |

| Chase | Existing customers | Broad mortgage offerings | Stricter underwriting possible |

| U.S. Bank | Conventional mortgages | Wide product selection | Regional availability limitations |

| SoFi | Digital-first borrowers | Online application experience | Strong credit often preferred |

| LightStream | Highly qualified borrowers | Competitive unsecured financing | Not a traditional mortgage specialist |

How Lenders Evaluate Home Loan Applications

- Credit score and history

- Payment history

- Income verification

- Employment history

- Debt-to-income ratio

- Assets and cash reserves

- Property appraisal

- Existing liabilities

- Down payment source

Home Loan Application Process

1. Prequalification

Estimate affordability and borrowing capacity.

2. Preapproval

Submit financial information for preliminary underwriting.

3. Home Search

Identify a property within your approved budget.

4. Formal Application

Provide documentation, including income and asset verification.

5. Underwriting

The lender evaluates creditworthiness and collateral.

6. Property Appraisal

An independent appraisal determines property value.

7. Closing and Funding

Sign final documents and complete the purchase.

How to Improve Approval Odds

- Improve your credit score before applying.

- Reduce outstanding debt.

- Increase your down payment.

- Maintain stable employment.

- Avoid opening new credit accounts before closing.

- Build emergency savings reserves.

Responsible Borrowing Tips

- Borrow within your long-term budget.

- Consider total housing costs, including taxes and insurance.

- Compare offers from multiple lenders.

- Review loan estimates carefully.

- Maintain an emergency fund after purchase.

Potential Risks of Home Loans

- Foreclosure risk if payments are missed

- Property value declines

- Rising costs for taxes and insurance

- Interest rate increases on adjustable-rate loans

- Reduced financial flexibility due to high debt

State and Local Considerations

Mortgage regulations, licensing requirements, foreclosure laws, and consumer protections vary by state. Certain loan products may not be available in all jurisdictions.

Frequently Asked Questions

1. What credit score is needed for a home loan?

Requirements vary by lender and loan program, but stronger credit profiles often qualify for better rates.

2. How much down payment is required?

Down payment requirements can range from 3% to 20% or more depending on the loan type.

3. What is APR?

APR reflects the total annual borrowing cost, including interest and certain fees.

4. How long does home loan approval take?

Mortgage approvals commonly take between 30 and 60 days.

5. Are home loans secured?

Yes. The property serves as collateral.

6. Can first-time buyers qualify?

Yes. Numerous loan programs are designed for first-time homebuyers.

7. Can I refinance my mortgage?

Many homeowners refinance to lower rates, reduce payments, or change loan terms.

8. What closing costs should I expect?

Closing costs often range from 2% to 6% of the home’s purchase price.

9. Should I get preapproved before shopping?

Preapproval can help establish a realistic budget and strengthen purchase offers.

10. Should I compare multiple lenders?

Comparing lenders may help borrowers identify competitive rates and fees.

Related Topics

- First-Time Home Buyer Loan Guide

- Best Mortgage Broker

- Best Commercial Mortgage Lenders

- Best Mortgage Lenders

- Investment Property Loan Guide

- VA Loan Guide

- FHA Loan Guide

- Mortgage Preapproval Checklist