Federal student loans remain one of the primary ways students finance higher education in the United States. Compared with many private education loans, federal loans often provide lower borrowing costs, fixed interest rates, flexible repayment options, and valuable borrower protections.

Understanding how federal student loans work can help students and families make informed decisions about college financing while minimizing long-term debt risks.

This guide explains eligibility requirements, loan types, interest rates, repayment options, and the application process for federal education loans.

Federal Student Loans Guide 2026: Rates, Eligibility & Repayment Options

Federal student loans are education loans funded by the U.S. Department of Education to help eligible students and parents pay qualified educational expenses.

Unlike many private loans, federal loans typically do not require extensive credit checks and may provide access to income-driven repayment plans, deferment, forbearance, and loan forgiveness programs.

Who Should Consider Federal Student Loans?

- Undergraduate students attending eligible schools

- Graduate and professional students

- Students with demonstrated financial need

- Families seeking flexible repayment options

- Borrowers looking for government borrower protections

What Expenses Can Federal Student Loans Cover?

Federal student loans may help pay for:

- Tuition and mandatory fees

- Housing and meal plans

- Books and academic supplies

- Technology and equipment

- Transportation expenses

- Other eligible educational costs

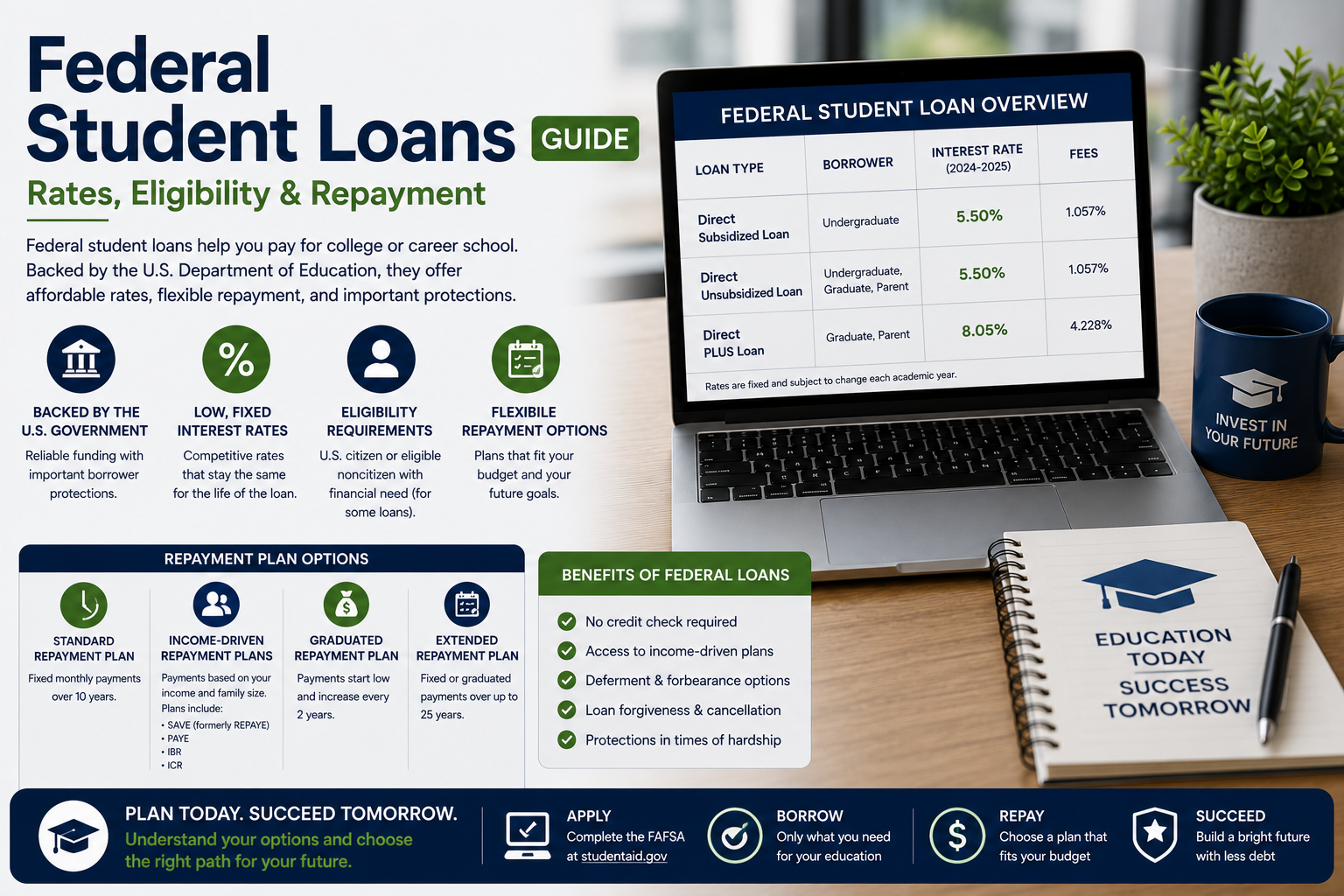

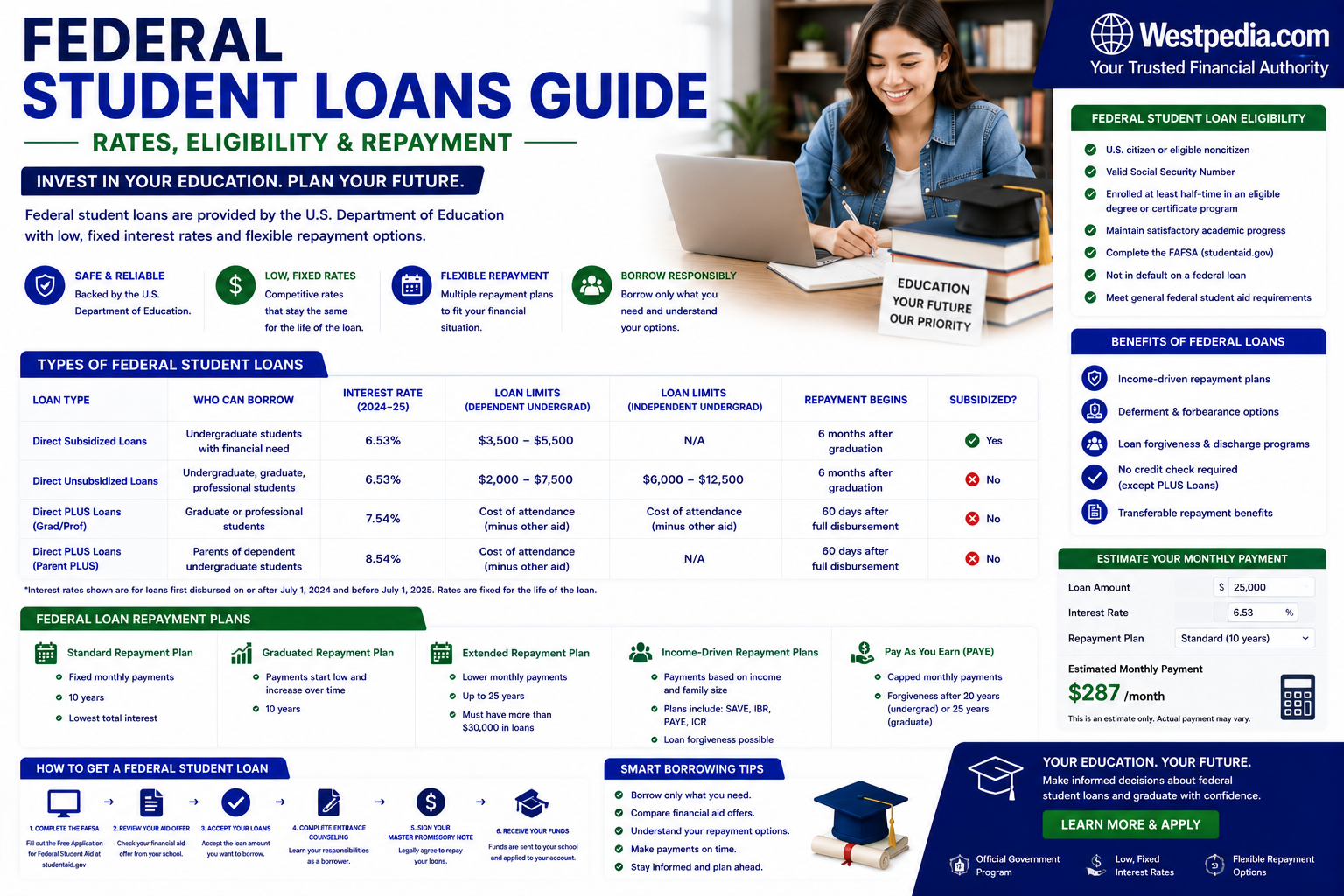

Types of Federal Student Loans

| Loan Program | Best For | Financial Need Required |

|---|---|---|

| Direct Subsidized Loans | Eligible undergraduate students | Yes |

| Direct Unsubsidized Loans | Undergraduate and graduate students | No |

| Direct PLUS Loans | Parents and graduate students | No |

| Direct Consolidation Loans | Borrowers combining federal loans | No |

Federal Student Loan Costs and Terms

| Feature | Typical Characteristics |

|---|---|

| Interest Rate Structure | Fixed Rates |

| Loan Terms | 10–30 Years Depending on Repayment Plan |

| Origination Fees | May Apply to Certain Loan Types |

| Grace Period | Typically Six Months After Leaving School |

| Prepayment Penalty | None |

| Credit Check | Generally Not Required for Most Student Loans |

Direct Subsidized Loans Explained

Direct Subsidized Loans are available to eligible undergraduate students who demonstrate financial need.

The government pays interest on subsidized loans while the student:

- Attends school at least half-time.

- Is within the grace period after leaving school.

- Qualifies for certain deferment periods.

Because interest costs may be lower, subsidized loans are often considered among the most favorable student borrowing options.

Direct Unsubsidized Loans Explained

Direct Unsubsidized Loans are available to eligible undergraduate, graduate, and professional students regardless of financial need.

Interest accrues from the time funds are disbursed, including while students remain enrolled.

PLUS Loans Explained

PLUS Loans are designed for:

- Graduate and professional students.

- Parents of dependent undergraduate students.

PLUS Loans typically require a limited credit review and may permit borrowing up to the school’s certified cost of attendance, less other financial aid received.

Annual and Aggregate Borrowing Limits

| Borrower Type | Typical Annual Limits |

|---|---|

| Dependent Undergraduate Students | Varies by academic year |

| Independent Undergraduate Students | Higher limits may apply |

| Graduate Students | Program-specific limits |

| PLUS Borrowers | Up to cost of attendance minus other aid |

Eligibility Requirements

Federal loan eligibility generally requires borrowers to:

- Complete applicable financial aid applications.

- Be enrolled or accepted at an eligible institution.

- Meet citizenship or eligible noncitizen requirements.

- Maintain satisfactory academic progress.

- Possess a valid Social Security number in most circumstances.

- Use loan funds for educational purposes.

How the Government Evaluates Borrowers

Federal student loan underwriting differs significantly from private lending.

- Financial need assessment

- Enrollment status

- Academic standing

- School certification

- Prior federal loan history

- Credit review for PLUS Loans only

Repayment Plan Options

| Repayment Plan | Borrower Fit | Key Benefit |

|---|---|---|

| Standard Repayment | Borrowers seeking faster payoff | Lower total interest costs |

| Graduated Repayment | Borrowers expecting income growth | Lower initial payments |

| Extended Repayment | Borrowers with larger balances | Reduced monthly payments |

| Income-Driven Repayment | Borrowers needing payment flexibility | Payments based on income |

Borrower Protections and Benefits

Federal student loans may provide important protections unavailable with many private loans.

- Income-driven repayment plans

- Deferment options

- Forbearance options

- Loan forgiveness programs

- Discharge provisions under qualifying circumstances

- No prepayment penalties

Loan Forgiveness Opportunities

Certain borrowers may qualify for federal loan forgiveness programs, subject to program rules and eligibility requirements.

Examples include:

- Public service-based forgiveness programs

- Teacher-focused forgiveness programs

- Income-driven repayment forgiveness provisions

Borrowers should carefully review program requirements before relying on potential forgiveness benefits.

Federal Student Loan Application Process

1. Complete Financial Aid Applications

Students begin by submitting required federal financial aid documentation.

2. Receive Financial Aid Offer

Schools provide aid packages detailing available grants, scholarships, and loans.

3. Review Loan Options

Borrowers should compare available aid before accepting loans.

4. Accept Desired Loan Amounts

Students can often choose whether to accept all or only part of offered aid.

5. Complete Entrance Counseling

First-time borrowers may need to complete educational requirements regarding loan responsibilities.

6. Sign Required Documentation

Borrowers must complete required loan agreements.

7. School Certification and Disbursement

Funds are typically sent directly to the educational institution.

How to Borrow Responsibly

- Maximize scholarships and grants first.

- Borrow only necessary amounts.

- Estimate future monthly payments.

- Understand total repayment obligations.

- Track cumulative borrowing throughout school.

Potential Risks of Student Borrowing

- Long-term debt obligations

- Interest accumulation

- Reduced financial flexibility after graduation

- Credit score damage from missed payments

- Challenges managing excessive debt balances

Federal vs. Private Student Loans

| Feature | Federal Loans | Private Loans |

|---|---|---|

| Interest Rate Structure | Fixed | Fixed or Variable |

| Credit Requirements | Limited | Common |

| Income-Based Repayment | Available | Limited |

| Forgiveness Opportunities | Available | Rare |

| Borrower Protections | Extensive | More Limited |

State and Regulatory Considerations

Federal student loans are governed primarily by federal law, although additional borrower protections, servicing regulations, and consumer protections may vary by state.

Frequently Asked Questions

1. What are federal student loans?

They are government-funded education loans designed to help eligible students pay college expenses.

2. Do federal student loans require a credit check?

Most federal student loans do not require traditional credit underwriting, although PLUS Loans generally include a limited credit review.

3. Are interest rates fixed?

Yes. Federal student loans generally carry fixed interest rates.

4. What is the grace period?

Many federal loans provide a six-month grace period after leaving school or dropping below half-time enrollment.

5. Can loans be forgiven?

Certain borrowers may qualify for forgiveness programs if specific requirements are met.

6. Are there prepayment penalties?

No. Borrowers may generally repay federal student loans early without penalties.

7. What is an income-driven repayment plan?

These plans base monthly payments on income and family size.

8. Can graduate students borrow federal loans?

Yes. Graduate students may qualify for unsubsidized and PLUS Loans.

9. Should federal loans be used before private loans?

Many financial aid professionals recommend exploring federal aid options first because of borrower protections.

10. How do students apply?

Students begin by completing required federal financial aid applications.

Related Topics

- Best Student Loans

- Private Student Loans

- Student Loan Refinance Guide

- Parent PLUS Loans

- Graduate Student Loans

- Student Loan Consolidation

- FAFSA Guide

- College Financial Aid Planning