Hyou can compare Best Student Loans Rates, Terms & Top Lenders. Paying for higher education continues to be one of the largest financial challenges facing students and families. Tuition costs, housing expenses, books, and other educational fees can add significant financial pressure, making student loans an important financing tool for many borrowers.

Choosing among the best student loans requires more than simply comparing interest rates. Borrowers should evaluate repayment flexibility, borrower protections, eligibility standards, cosigner requirements, and long-term affordability before committing to any education financing option.

This guide compares federal and private student loan options, explains how lenders evaluate applicants, and outlines strategies for borrowing responsibly.

What Are Student Loans?

Student loans are financing products designed to help borrowers pay qualified educational expenses, including tuition, housing, meal plans, books, supplies, and certain living costs.

Student financing generally falls into two categories:

- Federal student loans issued through government programs.

- Private student loans offered by banks, credit unions, and online lenders.

Who Should Consider Student Loans?

- Undergraduate students

- Graduate and professional students

- Parents helping finance education

- Borrowers attending accredited institutions

- Students who have exhausted scholarships and grants

What Financial Problem Do Student Loans Solve?

Student loans provide funding when personal savings, scholarships, grants, and family contributions are insufficient to cover educational costs.

Loans may help finance:

- Tuition and fees

- Room and board

- Books and supplies

- Technology expenses

- Transportation costs

- Professional program expenses

Federal vs. Private Student Loans

| Feature | Federal Student Loans | Private Student Loans |

|---|---|---|

| Credit Check | Usually Not Required | Often Required |

| Interest Rates | Government Set | Lender Determined |

| Repayment Flexibility | Extensive | Varies by Lender |

| Income-Driven Repayment | Available | Rare |

| Cosigner Requirement | Usually Not Required | Common |

| Borrower Protections | Strong | Limited |

Typical Student Loan Costs and Terms

| Feature | Typical Range |

|---|---|

| Loan Amount | $1,000 to Cost of Attendance |

| APR | 4% – 16%+ |

| Repayment Term | 5 – 25 Years |

| Origination Fee | 0% – 4%+ |

| Grace Period | 6 – 9 Months Common |

| Funding Timeline | Several Days to Several Weeks |

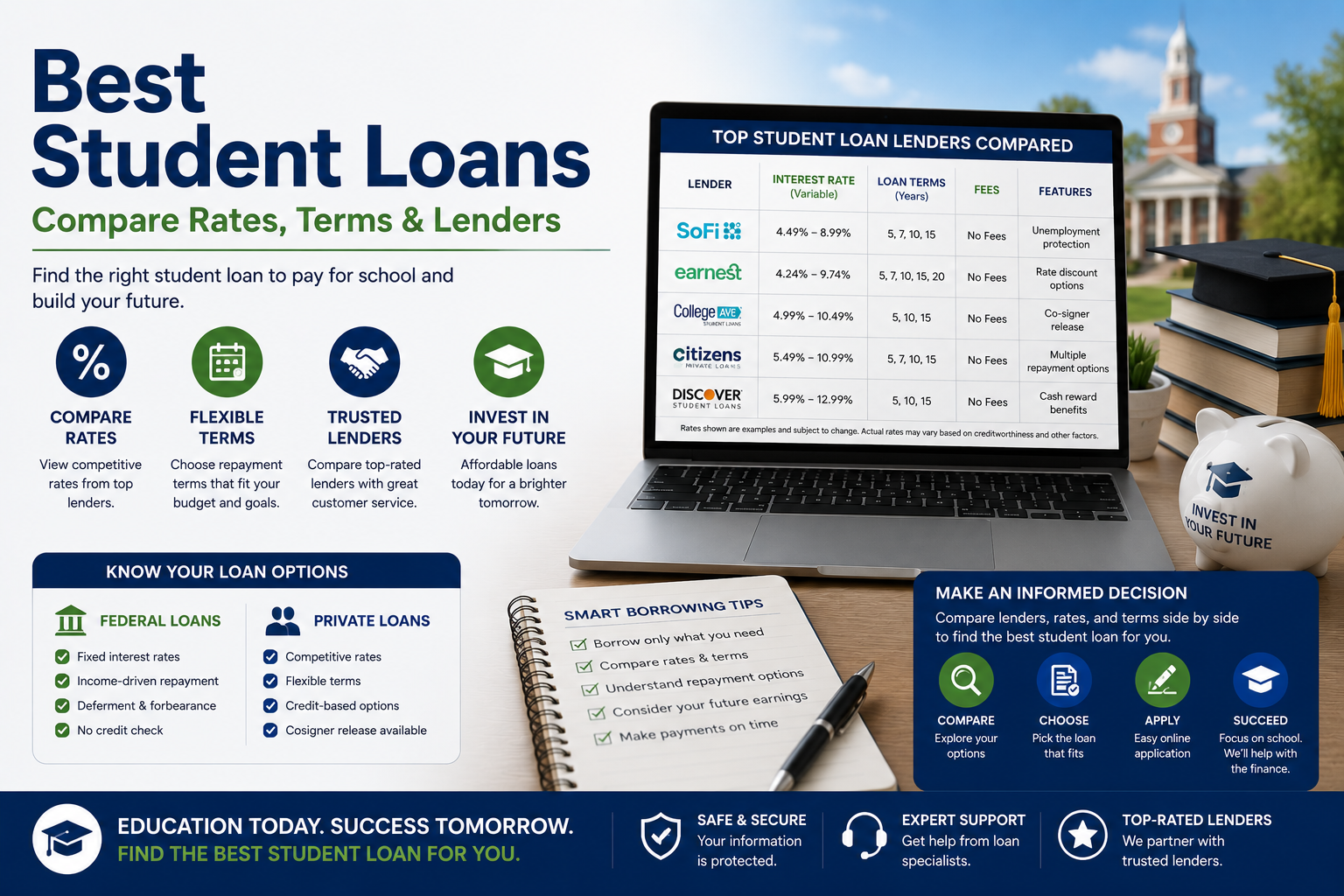

Best Student Loan Lenders Compared

| Lender | Best For | Strengths | Potential Limitations |

|---|---|---|---|

| SoFi | Graduate Borrowers | No fees, member benefits | Strong credit requirements |

| College Ave | Flexible repayment | Customizable loan terms | Cosigner may be needed |

| Sallie Mae | Wide borrower eligibility | Multiple education loan products | Rates may be higher for some borrowers |

| Earnest | Financially strong applicants | Flexible repayment options | Strict underwriting standards |

| Discover Student Loans | No-fee borrowing | No application or origination fees | Limited repayment customization |

| Citizens Bank | Existing banking customers | Relationship discounts available | Competitive credit standards |

| LendingClub | Refinancing alternatives | Consumer lending experience | Limited traditional student lending |

| LightStream | Highly qualified borrowers | Competitive unsecured financing | Not a dedicated student lender |

Federal Student Loan Programs

| Program | Best For | Credit Requirement |

|---|---|---|

| Direct Subsidized Loans | Undergraduates with financial need | No |

| Direct Unsubsidized Loans | Most students | No |

| PLUS Loans | Parents and graduate students | Limited credit review |

| Consolidation Loans | Federal loan simplification | No |

How Lenders Evaluate Student Loan Applicants

Private lenders commonly assess:

- Credit score

- Credit history

- Payment history

- Income level

- Employment history

- Debt-to-income ratio (DTI)

- Cosigner strength

- School eligibility

- Degree program

- Expected graduation date

Credit Score Requirements

Private lenders establish their own qualification standards.

- Excellent Credit: 720+

- Good Credit: 680–719

- Fair Credit: 640–679

- Limited Credit: Cosigner frequently recommended

Many undergraduate students rely on cosigners because they have limited credit histories.

Fixed-Rate vs. Variable-Rate Student Loans

| Loan Type | Advantages | Potential Risks |

|---|---|---|

| Fixed Rate | Predictable monthly payments | Higher initial rate possible |

| Variable Rate | Lower starting rate potential | Payments may increase over time |

How to Apply for Student Loans

1. Complete Financial Aid Applications

Students should generally submit applicable financial aid forms before considering private borrowing.

2. Review Scholarships and Grants

Maximize non-repayable aid first.

3. Compare Loan Offers

Evaluate APRs, repayment options, fees, and borrower protections.

4. Prequalify if Available

Some private lenders offer rate estimates without affecting credit scores.

5. Submit an Application

Provide required personal, academic, and financial information.

6. Underwriting Review

The lender evaluates borrower qualifications and cosigner information if applicable.

7. School Certification and Funding

The educational institution confirms enrollment before funds are disbursed.

How to Improve Approval Odds

- Apply with a creditworthy cosigner.

- Build credit before borrowing.

- Maintain on-time payments on existing accounts.

- Reduce outstanding debt.

- Compare multiple lenders.

- Borrow only necessary amounts.

Responsible Borrowing Strategies

- Prioritize grants and scholarships.

- Use federal loans before private loans when appropriate.

- Borrow only what is necessary.

- Estimate future monthly payments before accepting loans.

- Understand repayment obligations before signing.

Potential Risks of Student Loan Borrowing

- Long-term debt obligations

- Interest accumulation

- Payment difficulties after graduation

- Credit score damage from missed payments

- Limited bankruptcy discharge options

State and Regulatory Considerations

Student lending laws, servicing regulations, borrower protections, and refinancing availability may vary by state. Certain loan products and lender programs may not be offered in every jurisdiction. Borrowers exploring real estate financing may also consider an Investment Property Loan, while evaluating Best Liability Insurance Providers to help ensure adequate protection against potential legal and financial risks.

Frequently Asked Questions

1. What are the Top student loans?

The best option depends on individual circumstances, but federal student loans are generally recommended before private borrowing.

2. Should I choose federal or private loans?

Federal loans often provide stronger borrower protections and flexible repayment options.

3. What credit score is needed for private student loans?

Requirements vary, but stronger credit profiles may qualify for better rates.

4. Do student loans require collateral?

Most student loans are unsecured and do not require collateral.

5. Can I apply without a cosigner?

Yes, although some private lenders may require or recommend one.

6. How long does approval take?

Approval timelines range from several days to several weeks.

7. What is APR?

APR reflects the total annual borrowing cost, including interest and certain fees.

8. Can student loans be refinanced?

Many private lenders offer student loan refinancing options.

9. Are there fees?

Some loans include origination or late-payment fees, while others do not.

10. Should I compare lenders?

Yes. Comparing multiple lenders can help borrowers evaluate rates, terms, and repayment flexibility.

Related Topics

- Student Loan Refinance Guide

- Private Student Loans

- Federal Student Loan Programs

- Graduate Student Loans

- Parent PLUS Loans

- Student Loan Consolidation

- Education Financing Strategies

- Scholarships and Grants Guide