Investment Property Loan Guide their Rates, Requirements & Best Lenders. Real estate investing remains one of the most popular ways to build long-term wealth, generate passive income, and diversify investment portfolios. Whether you plan to purchase a single-family rental home, a multi-unit property, or refinance an existing investment, choosing the right financing solution is critical.

An investment property loan differs significantly from a mortgage used to buy a primary residence. Lenders generally impose stricter underwriting standards because investment properties typically present greater risk. Understanding rates, down payment requirements, lender expectations, and available financing options can help investors make informed borrowing decisions.

What Is an Investment Property Loan?

An investment property loan is a mortgage or real estate financing product used to purchase, refinance, or improve property intended to generate rental income or investment returns rather than serve as the borrower’s primary residence.

Common investment properties include:

- Single-family rental homes

- Multi-family properties

- Vacation rentals

- Condominium rentals

- Small apartment buildings

- Commercial investment properties

Who Should Consider an Investment Property Loan?

- First-time real estate investors

- Experienced landlords

- Property flippers

- Buy-and-hold investors

- Vacation rental owners

- Individuals seeking passive income

What Financial Problem Does This Loan Solve?

Investment real estate often requires substantial capital. Financing enables investors to:

- Acquire rental properties without paying entirely in cash.

- Expand real estate portfolios.

- Preserve liquidity for renovations and reserves.

- Leverage capital to pursue multiple investment opportunities.

- Refinance existing investment properties.

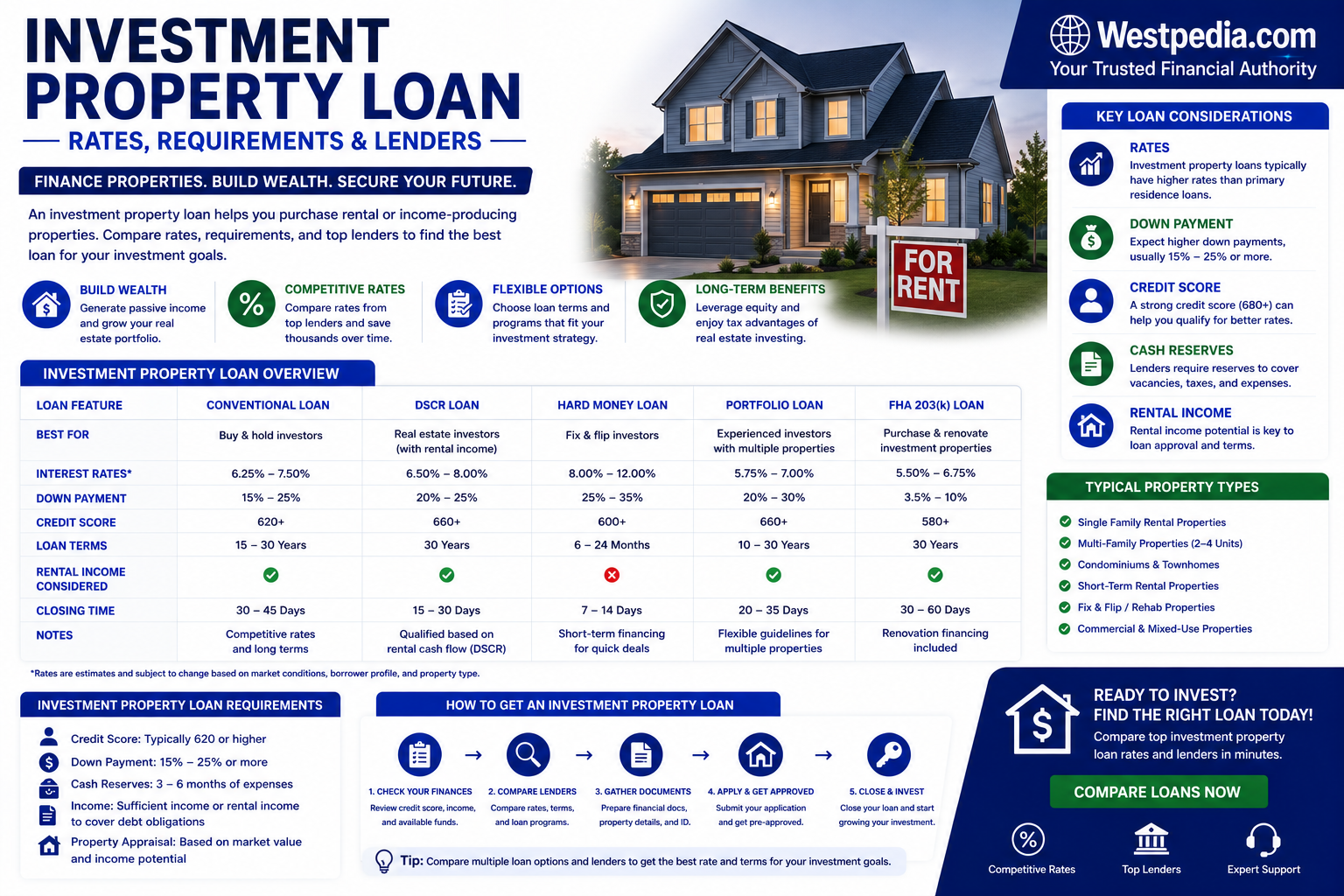

Investment Property Loan Costs, Rates & Terms

| Feature | Typical Range |

|---|---|

| Loan Amount | $75,000 to several million dollars |

| APR | 6.25% – 10.50% |

| Down Payment | 15% – 30%+ |

| Loan Terms | 10 – 30 years |

| Origination Fees | 0% – 3% |

| Closing Costs | 2% – 6% of loan amount |

Investment property mortgages generally carry higher interest rates than owner-occupied home loans because lenders assume greater default risk.

Types of Investment Property Financing

| Loan Type | Best For | Typical Down Payment | Key Considerations |

|---|---|---|---|

| Conventional Investment Mortgage | Long-term rental investors | 15%–25% | Competitive rates for qualified borrowers |

| DSCR Loan | Cash-flow investors | 20%–30% | Property income emphasized |

| Portfolio Loan | Multiple-property investors | 20%–30% | Flexible underwriting |

| Commercial Real Estate Loan | Large investment properties | 20%–35% | Business-oriented underwriting |

| Hard Money Loan | Fix-and-flip investors | 10%–30% | Short-term financing with higher rates |

| Home Equity Loan | Existing homeowners | Varies | Uses existing home equity |

Typical Borrower Profiles

Lenders commonly finance borrowers with:

- Strong personal credit histories

- Documented rental income experience

- Sufficient cash reserves

- Stable employment or business income

- Manageable debt obligations

Real-World Borrowing Scenarios

- Purchasing a first rental property.

- Acquiring a duplex or fourplex.

- Expanding a real estate portfolio.

- Refinancing an investment property to lower monthly payments.

- Purchasing a short-term vacation rental.

Factors That Influence Investment Property Rates

Lenders evaluate several risk factors when pricing investment loans.

- Credit Score: Higher scores generally qualify for better rates.

- Debt-to-Income Ratio: Lower DTI ratios often improve eligibility.

- Cash Reserves: Many lenders require six to twelve months of reserves.

- Property Type: Multi-unit and vacation rentals may carry additional risk.

- Down Payment: Larger down payments may reduce borrowing costs.

- Loan Amount: Jumbo financing may involve different pricing.

- Occupancy Status: Non-owner-occupied properties usually have higher rates.

- Geographic Market: Local market conditions can affect loan availability.

Down Payment Requirements

Most lenders require larger down payments for investment properties than primary residences.

| Property Type | Typical Minimum Down Payment |

|---|---|

| Single-Family Rental | 15%–20% |

| Two-to-Four Unit Property | 20%–25% |

| Vacation Rental | 20%–30% |

| Commercial Property | 20%–35% |

Best Lenders for Investment Property Financing

| Lender | Best For | Strengths | Potential Limitations |

|---|---|---|---|

| Bank of America | Relationship banking | Established mortgage platform | Conservative underwriting |

| Wells Fargo | Traditional investors | National mortgage network | Detailed documentation requirements |

| Chase | Existing banking customers | Broad mortgage products | Stricter qualification standards |

| U.S. Bank | Conventional investment loans | Diverse financing solutions | Availability varies by region |

| SoFi | Digital borrowers | Online experience | Limited investment property offerings |

| LendingClub | Supplemental financing | Personal loan solutions | Not a traditional mortgage lender |

| Funding Circle | Business real estate investors | Business financing expertise | Limited traditional mortgages |

| Live Oak Bank | Commercial investors | Business lending specialization | Limited residential investor focus |

How Lenders Underwrite Investment Property Loans

Underwriters evaluate both the borrower and the property.

- Personal credit score and history

- Payment history

- Debt-to-income ratio (DTI)

- Employment and income verification

- Existing mortgage obligations

- Cash reserves

- Rental income potential

- Property appraisal value

- Occupancy strategy

- Collateral quality

Secured vs. Unsecured Financing

Most investment property loans are secured by real estate collateral. Unsecured financing, such as personal loans or business loans, may occasionally supplement investment purchases but often carries higher borrowing costs and lower loan limits.

Fixed-Rate vs. Variable-Rate Loans

- Fixed-Rate Loans: Monthly principal and interest payments remain predictable.

- Variable-Rate Loans: Rates may fluctuate over time, potentially affecting cash flow.

Investment Property Loan Application Process

1. Prequalification

Estimate borrowing capacity and investment budget.

2. Property Identification

Select an investment property aligned with financial goals.

3. Formal Application

Submit personal and property documentation.

4. Documentation Review

Lenders review tax returns, bank statements, and financial records.

5. Underwriting

The lender assesses risk, collateral value, and repayment ability.

6. Appraisal

An independent appraisal determines market value.

7. Approval and Closing

Approved borrowers finalize documents and receive funding.

How to Improve Approval Odds

- Improve credit scores before applying.

- Reduce outstanding debt.

- Increase cash reserves.

- Save for a larger down payment.

- Maintain stable income.

- Prepare detailed investment projections.

Responsible Borrowing and Risk Management

Investment real estate carries financial risks. Borrowers should evaluate:

- Vacancy risk

- Maintenance expenses

- Property tax increases

- Insurance costs

- Market fluctuations

- Interest rate changes

Maintaining emergency reserves and realistic cash-flow assumptions can help reduce investment risk.

State and Local Lending Considerations

Mortgage licensing laws, foreclosure procedures, consumer protections, and investment property regulations vary by state. Certain loan products and programs may not be available in all jurisdictions.

Frequently Asked Questions

1. What credit score is needed for an investment property loan?

Many lenders prefer credit scores of 680 or higher, although requirements vary.

2. How much down payment is required?

Most investment property mortgages require at least 15% to 25% down.

3. Are interest rates higher for investment properties?

Yes. Investment properties typically carry higher rates than primary residences.

4. Can rental income help me qualify?

Many lenders may consider projected or documented rental income.

5. Are investment property loans secured?

Yes. Most are secured by the underlying real estate.

6. Can first-time investors qualify?

Yes, although additional documentation or reserves may be required.

7. How long does approval take?

Funding often takes 30 to 60 days, depending on complexity.

8. Are commercial properties financed differently?

Yes. Commercial loans typically involve business cash-flow analysis and different underwriting standards.

9. Can I refinance an investment property?

Yes. Investors frequently refinance to lower rates, change terms, or access equity.

10. Should I compare multiple lenders?

Comparing lenders can help investors evaluate rates, fees, and qualification requirements.

Related Topics

- SBA Loan Requirements

- Hard Money Loan Guide

- Rental Property Mortgage Guide

- DSCR Loan Guide

- Small Business Loan Guide

- Mortgage Refinance Guide

- Home Equity Loan Guide

- Real Estate Investment Strategies