Here is SBA Loan Requirements Eligibility, Credit & Approval Guide. Small Business Administration (SBA) loans remain one of the most affordable financing options available to entrepreneurs and small business owners. Because SBA loans are partially guaranteed by the federal government, lenders may offer competitive interest rates, longer repayment terms, and higher borrowing limits than many alternative financing products.

However, SBA financing involves detailed underwriting standards. Understanding SBA loan requirements before applying can help business owners improve approval odds, prepare documentation, and identify the most appropriate financing program.

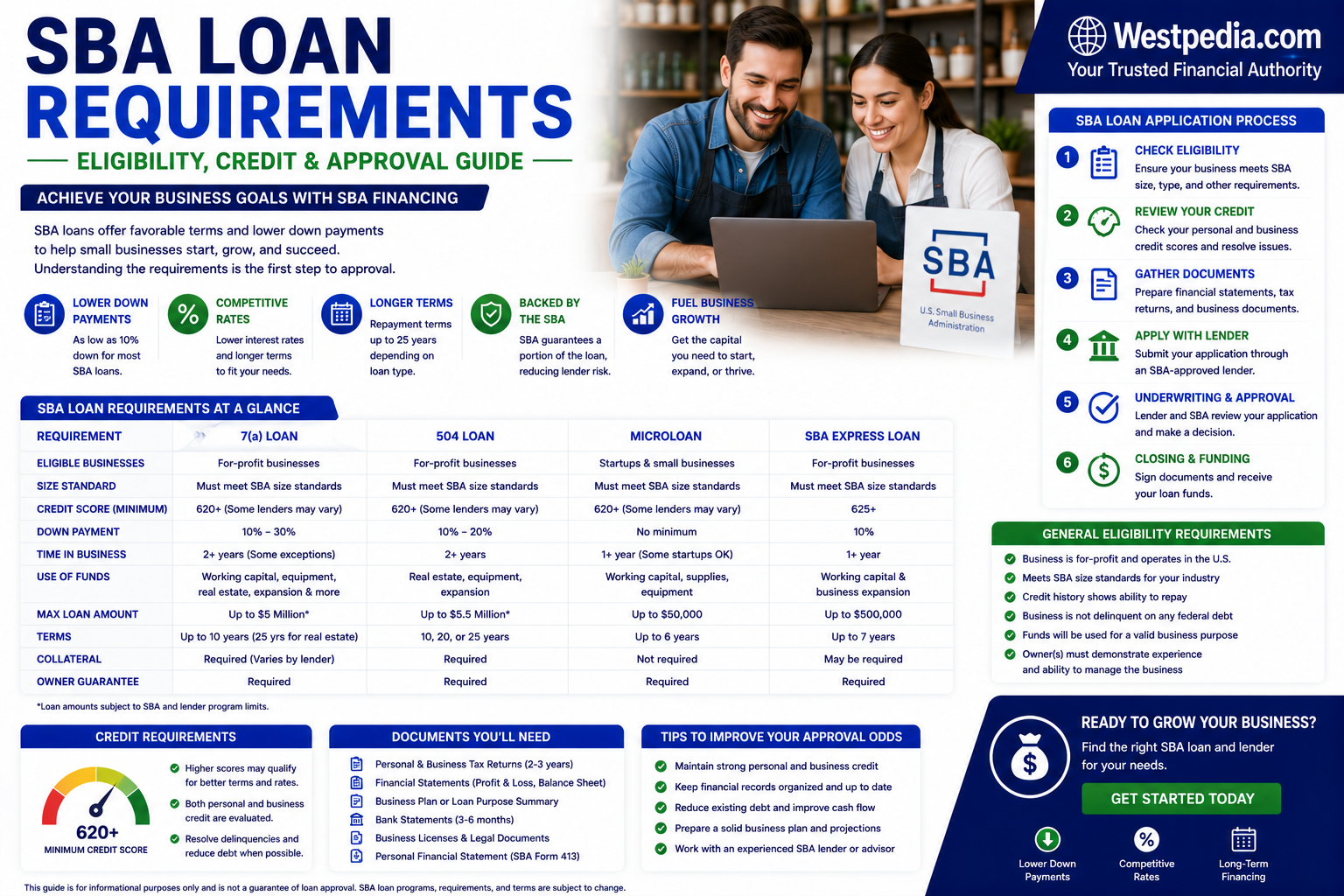

What Are SBA Loan Requirements?

SBA loan requirements are the qualification standards businesses must meet to be considered for financing through SBA-backed lending programs. Although requirements vary among lenders and loan programs, most applicants must satisfy both SBA eligibility rules and lender-specific underwriting guidelines.

Common SBA programs include:

- SBA 7(a) Loans

- SBA 504 Loans

- SBA Express Loans

- SBA Microloans

- SBA CAPLines

Who Should Consider an SBA Loan?

- Established small businesses

- Business owners seeking long repayment terms

- Companies purchasing commercial real estate

- Businesses acquiring equipment

- Entrepreneurs refinancing business debt

- Companies seeking working capital

- Businesses expanding operations

Basic SBA Eligibility Requirements

Most businesses must meet the following minimum standards:

- Operate as a for-profit business.

- Conduct business primarily within the United States.

- Meet SBA size standards.

- Demonstrate a legitimate business purpose.

- Show reasonable ability to repay debt.

- Invest owner equity in the business.

- Seek financing that cannot be obtained on reasonable terms elsewhere.

Core SBA Loan Requirements at a Glance

| Requirement | Typical Expectation |

|---|---|

| Business Type | For-profit U.S. business |

| Credit Score | Generally 650+ |

| Time in Business | Often 2+ years preferred |

| Business Revenue | Sufficient to support repayment |

| Cash Flow | Positive and stable |

| Collateral | May be required |

| Owner Equity | Required in many cases |

| Personal Guarantee | Typically required for owners with 20%+ ownership |

Minimum Credit Score Requirements

The SBA itself does not establish a universal minimum credit score. Individual lenders determine acceptable credit standards.

| SBA Program | Typical Credit Range | Borrower Profile |

|---|---|---|

| SBA 7(a) | 650–700+ | Established Businesses |

| SBA Express | 650–680+ | Working Capital Borrowers |

| SBA 504 | 680+ | Commercial Real Estate Borrowers |

| SBA Microloan | Flexible | Startups and Smaller Businesses |

Higher credit scores often improve approval odds and may help borrowers secure more favorable loan terms.

Business Revenue Requirements

Lenders evaluate whether the business generates enough revenue to comfortably repay debt obligations.

Key revenue considerations include:

- Annual gross revenue

- Net operating income

- Profit margins

- Revenue consistency

- Industry performance

- Seasonality trends

There is no universal minimum revenue requirement. Instead, lenders analyze whether projected cash flow adequately supports loan repayment.

Cash Flow and Debt Service Coverage Ratio (DSCR)

Cash flow is among the most important SBA underwriting factors.

Lenders frequently calculate the Debt Service Coverage Ratio (DSCR).

- DSCR above 1.25x is commonly preferred.

- Higher ratios generally indicate stronger repayment capacity.

Businesses with inconsistent cash flow may face additional underwriting scrutiny.

Collateral Requirements

Collateral requirements depend on the loan amount, lender policies, and available business assets.

Collateral may include:

- Commercial real estate

- Equipment

- Inventory

- Accounts receivable

- Business assets

- Personal assets in some circumstances

Insufficient collateral does not automatically disqualify applicants, particularly for certain SBA programs.

Personal Guarantee Requirements

Most SBA lenders require personal guarantees from owners with at least 20% ownership interest in the business.

A personal guarantee means owners may become personally responsible for repayment if the business cannot satisfy its debt obligations.

Time in Business Requirements

| Business Stage | Financing Considerations |

|---|---|

| Startup Businesses | May require stronger financials and larger equity injections |

| 1–2 Years in Business | Additional documentation often required |

| 2+ Years in Business | Often preferred by lenders |

| Established Businesses | Typically viewed more favorably |

Industries That May Face Restrictions

Certain businesses may be ineligible or subject to additional review.

Examples can include:

- Speculative businesses

- Illegal businesses

- Certain passive investment businesses

- Pyramid sales organizations

- Businesses engaged primarily in lending activities

Documentation Required for SBA Loan Approval

Most applicants should expect to provide:

- Business plan

- Personal tax returns

- Business tax returns

- Financial statements

- Profit and loss statements

- Balance sheets

- Business licenses

- Bank statements

- Debt schedule

- Legal formation documents

- Ownership information

- Resume or management experience documentation

How Lenders Evaluate SBA Borrowers

- Credit score and credit history

- Payment history

- Business revenue

- Cash flow performance

- Debt obligations

- Management experience

- Industry risk

- Collateral value

- Business plan quality

- Financial trends

Major SBA Lenders Compared

| Lender | Best For | Strengths | Potential Limitations |

|---|---|---|---|

| Live Oak Bank | SBA Specialists | Extensive SBA Experience | Detailed Documentation Requirements |

| Bank of America | Established Businesses | National Lending Platform | Stricter Qualification Standards |

| Wells Fargo | Commercial Borrowers | Broad SBA Offerings | Longer Approval Process |

| Chase | Relationship Banking | Large Branch Network | Competitive Underwriting |

| U.S. Bank | Owner-Occupied Businesses | Diverse Loan Programs | Regional Availability Differences |

| Funding Circle | Alternative Business Financing | Fast Decisions | Limited SBA Focus |

| Bluevine | Working Capital | Digital Experience | Not a Major SBA Lender |

| OnDeck | Short-Term Business Financing | Speed | Higher Cost Alternatives |

SBA Loan Application Process

1. Prequalification

Review basic eligibility and financing needs.

2. Select an SBA Program

Determine whether SBA 7(a), 504, Express, or Microloan financing best fits your needs.

3. Gather Documentation

Compile financial statements, tax returns, and supporting business documents.

4. Submit Application

Provide all required forms and disclosures.

5. Underwriting Review

The lender evaluates repayment ability, risk profile, and SBA eligibility.

6. Approval Decision

Approved applicants receive loan terms and disclosures.

7. Funding

Funding timelines vary by lender and loan complexity.

How to Improve SBA Loan Approval Odds

- Improve personal and business credit scores.

- Reduce existing debt obligations.

- Strengthen business cash flow.

- Prepare a detailed business plan.

- Maintain organized financial records.

- Increase owner equity contributions.

- Correct inaccuracies on credit reports.

Responsible Borrowing Considerations

- Borrow only what your business can reasonably repay.

- Evaluate future cash-flow projections carefully.

- Maintain adequate operating reserves.

- Compare multiple lenders before applying.

State and Regulatory Considerations

Although SBA programs are federally supported, lender licensing requirements, collateral laws, foreclosure procedures, and certain consumer protections may vary by state. Loan availability may also differ among lenders and regions.

Frequently Asked Questions

1. What credit score is needed for an SBA loan?

Many lenders prefer scores of 650 or higher, although requirements vary.

2. Do startups qualify for SBA loans?

Some startups may qualify, but lenders often require stronger documentation and owner investment.

3. Is collateral required?

Collateral requirements depend on the loan amount and lender policies.

4. Are personal guarantees required?

Most owners with 20% or greater ownership interest are typically required to provide personal guarantees.

5. How long does approval take?

Approval timelines can range from several weeks to several months.

6. Can businesses with bad credit qualify?

Approval may still be possible, but stronger compensating factors are often necessary.

7. Are SBA loans available for working capital?

Yes. SBA 7(a) loans commonly support working capital needs.

8. What documents are required?

Financial statements, tax returns, business plans, and ownership information are commonly requested.

9. Does the SBA lend directly?

Most SBA loans are issued by participating lenders and partially guaranteed by the SBA.

10. Should I compare lenders?

Yes. Eligibility standards, fees, and approval processes vary among lenders.

Related Topics

- SBA 7(a) Loan Guide

- SBA Loan Calculator

- Small Business Loan Guide

- Commercial Real Estate Loan

- Business Line of Credit

- SBA 504 Loan Requirements

- Startup Business Loan Guide

- Working Capital Loan Guide