Life insurance is a contract between a policyholder and an insurer that provides a tax-advantaged death benefit to beneficiaries when the insured person dies. It helps families replace lost income, cover debts, pay final expenses, and achieve long-term financial security. Individuals with dependents, financial obligations, or estate-planning goals often consider life insurance an important part of financial protection.

Life Insurance: Complete Guide to Coverage, Costs, Policy Types & Providers

Life insurance is one of the most important financial tools available for protecting loved ones from financial hardship after the death of a family member. While many people understand the basic concept, choosing the right policy can be challenging due to the variety of coverage options, pricing structures, and underwriting requirements.

This guide explains how life insurance works, who needs it, policy types, costs, underwriting factors, major providers, claims processes, and practical considerations for comparing quotes.

What Is Life Insurance?

Life insurance is a legal contract in which an insurance company agrees to pay a death benefit to designated beneficiaries when the insured individual dies, provided policy terms and conditions are met.

In exchange, the policyholder pays premiums either monthly, quarterly, or annually.

The primary purpose of life insurance is financial protection for surviving family members and dependents.

Why Life Insurance Matters

Unexpected death can create significant financial challenges for families.

Life insurance can help beneficiaries:

- Replace lost income

- Pay mortgage obligations

- Cover education expenses

- Manage outstanding debts

- Pay final expenses

- Support long-term financial goals

- Preserve family assets

- Assist with estate planning objectives

Who Needs Life Insurance?

- Parents with dependent children

- Married couples

- Homeowners

- Business owners

- Individuals with outstanding debts

- High-income earners

- Estate planning households

- People supporting aging parents

Not everyone requires the same amount or type of life insurance, which is why individual financial circumstances should be evaluated carefully.

Life Insurance Coverage Comparison

| Policy Type | Coverage Duration | Cash Value | Typical Cost | Best For |

|---|---|---|---|---|

| Term Life Insurance | Fixed term | No | Lowest | Income replacement |

| Whole Life Insurance | Lifetime | Yes | High | Permanent protection |

| Universal Life Insurance | Lifetime | Yes | Moderate to High | Flexible premiums |

| Final Expense Insurance | Lifetime | Limited | Moderate | Burial costs |

| Guaranteed Issue Insurance | Lifetime | No | Highest | Applicants with health concerns |

Types of Life Insurance Explained

Term Life Insurance

Term life insurance provides coverage for a specific period, commonly 10, 20, or 30 years. It is often chosen for affordability and income replacement needs.

Whole Life Insurance

Whole life insurance offers permanent coverage and includes a cash value component that may grow over time.

Universal Life Insurance

Universal life policies combine permanent coverage with flexible premiums and adjustable death benefits.

Final Expense Insurance

Final expense policies are designed to help cover funeral and end-of-life expenses.

Guaranteed Issue Life Insurance

These policies typically require no medical examination but often have higher premiums and lower coverage limits.

How Much Does Life Insurance Cost?

Life insurance premiums vary significantly depending on personal risk factors and policy design.

| Applicant Profile | Risk Level | Estimated Monthly Cost Range |

|---|---|---|

| Young Healthy Adult | Low | $15–$50+ |

| Middle-Aged Adult | Moderate | $40–$150+ |

| Senior Applicant | Higher | $100–$500+ |

| High-Risk Health Profile | High | Varies significantly |

Actual premiums depend on underwriting results, insurer guidelines, policy type, and coverage amount.

Key Factors That Affect Life Insurance Premiums

- Age

- Health history

- Tobacco use

- Coverage amount

- Policy type

- Family medical history

- Occupation

- Lifestyle factors

- Hazardous hobbies

- Gender (where legally permitted)

How Life Insurance Underwriting Works

Life insurers evaluate applicants using underwriting processes designed to estimate mortality risk.

Medical History

Chronic conditions, prescriptions, and treatment history may affect eligibility and pricing.

Lifestyle Evaluation

Activities such as smoking, skydiving, or high-risk occupations may influence premiums.

Coverage Amount Requested

Larger death benefits generally require additional underwriting review.

Financial Review

Insurers may assess income and financial obligations when evaluating large coverage requests.

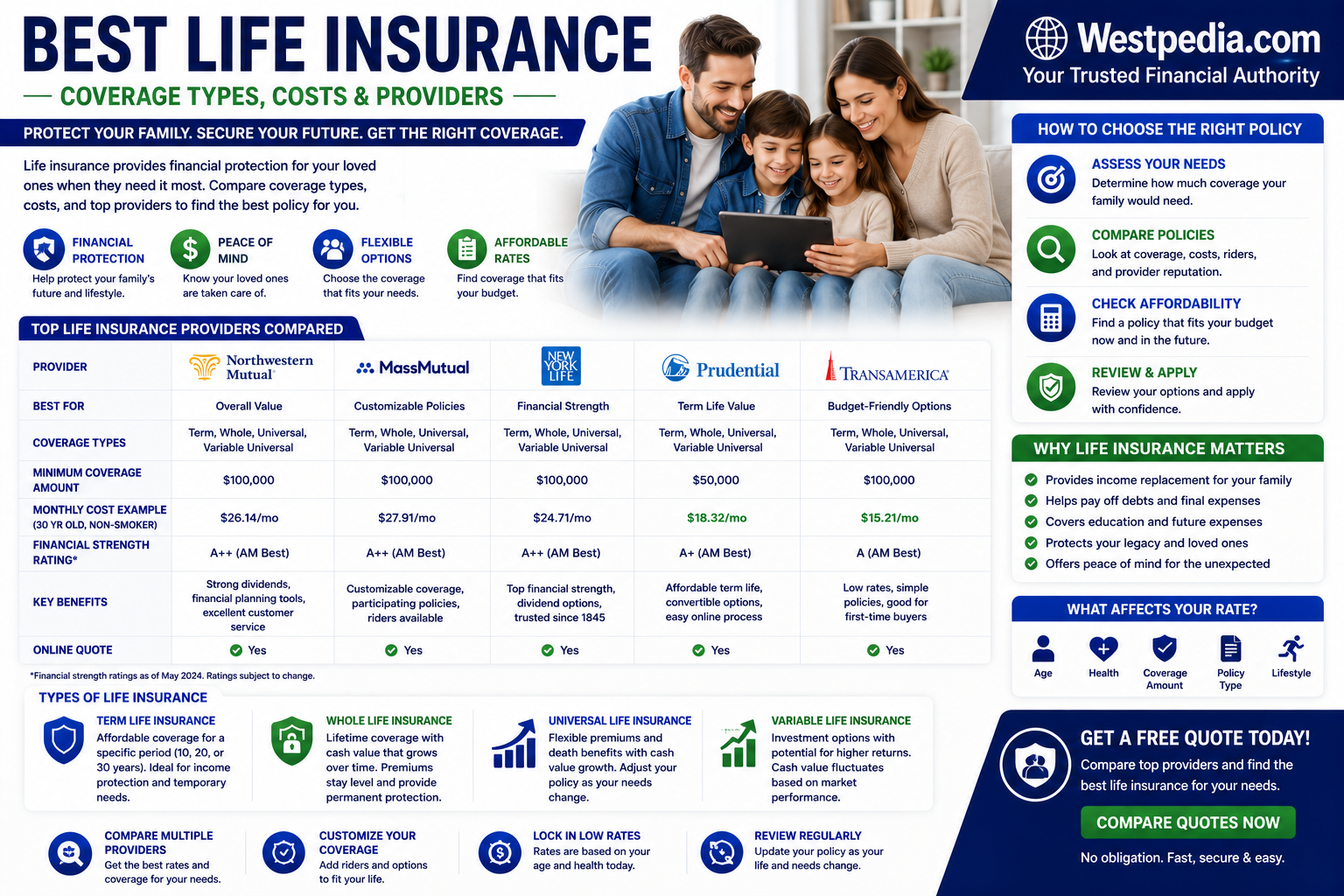

Life Insurance Provider Comparison

| Provider | Best For | Strengths | Potential Limitations | Pricing Position |

|---|---|---|---|---|

| Northwestern Mutual | Permanent coverage | Strong financial strength | Agent-based process | Premium |

| MassMutual | Whole life insurance | Strong participating policies | Higher premiums possible | Premium |

| New York Life | Comprehensive options | Long operating history | Agent-focused model | Mid to Premium |

| Guardian | Permanent protection | Strong policy customization | Availability varies | Premium |

| Prudential | Complex underwriting cases | Broad product lineup | Pricing varies significantly | Mid-range |

How the Life Insurance Claims Process Works

- The insured person passes away.

- The beneficiary contacts the insurance company.

- A claim form is completed.

- A certified death certificate is submitted.

- The insurer reviews the claim.

- The death benefit is approved if policy requirements are satisfied.

- The benefit is paid to beneficiaries.

How to Reduce Life Insurance Costs

- Apply at a younger age

- Maintain good health

- Avoid tobacco products

- Compare multiple quotes

- Choose appropriate coverage amounts

- Consider term insurance when suitable

- Review policies periodically

Common Life Insurance Mistakes

- Waiting too long to apply

- Purchasing insufficient coverage

- Failing to update beneficiaries

- Choosing solely based on price

- Ignoring policy exclusions

- Misrepresenting health information

Expert Considerations Before Buying

Before requesting life insurance quotes, evaluate financial obligations, family needs, future income replacement requirements, estate planning goals, and debt responsibilities.

Comparing policy types, insurer financial strength, premium affordability, and coverage flexibility can help support better long-term decisions. Consumers and business owners may also benefit from researching the Best Commercial Auto Insurance options for business vehicles while comparing Cheap Car Insurance policies that balance affordability with adequate protection.

Frequently Asked Questions

1. What does life insurance cover?

Life insurance pays a death benefit to beneficiaries after the insured person dies.

2. How much life insurance do I need?

Coverage needs vary based on income, debts, dependents, and financial goals.

3. Is term life insurance better than whole life insurance?

Neither is universally better; suitability depends on personal objectives and budget.

4. Can I buy life insurance without a medical exam?

Some insurers offer simplified issue and no-exam policies.

5. Are life insurance benefits taxable?

Death benefits are often tax-advantaged, though specific situations may vary.

6. What happens if I miss premium payments?

Coverage may lapse depending on policy provisions and grace periods.

7. Who should be a beneficiary?

Beneficiaries are chosen by the policyholder and may include family members, trusts, or organizations.

8. Can beneficiaries be changed?

Many policies allow beneficiary changes, subject to policy terms.

9. What is cash value?

Cash value is a savings component available in certain permanent life insurance policies.

10. When should I buy life insurance?

Many individuals obtain coverage when they have dependents or significant financial obligations.

11. Does life insurance cover accidental death?

Most policies cover accidental death, subject to policy terms and exclusions.

12. How long does a claim take?

Processing times vary depending on documentation and claim complexity.

Related Topics

- Term Life Insurance

- Whole Life Insurance

- Universal Life Insurance

- Final Expense Insurance

- Estate Planning